Summary. The BIR 2307 form, or Certificate of Creditable Tax Withheld at Source, is a crucial compliance document in the Philippines that confirms taxes withheld and remitted to the Bureau of Internal Revenue (BIR) for payments made to contractors, suppliers, and professionals. Managing the BIR Form 2307 manually can be time-consuming and prone to costly errors, but with Omni’s HR and payroll automation, teams can simplify compliance. Omni automatically applies the correct tax rates, generates digital 2307 BIR forms, and keeps all records centralized and audit-ready. Designed for modern, growing teams across APAC, Omni helps HR and finance teams stay compliant, reduce manual work, and gain confidence in every filing.

For HR managers, finance teams, and business owners in the Philippines, managing withholding taxes and ensuring all documentation for the Bureau of Internal Revenue (BIR) is accurate can feel like an unending compliance chore. The proper handling of the BIR 2307 form is a critical, and often challenging, part of this process.

The BIR Form 2307 is officially titled the Certificate of Creditable Tax Withheld at Source. It's a mandatory document required whenever you pay certain professionals, contractors, or suppliers. For the business making the payment, issuing this form serves as proof that you have withheld a portion of the payment as tax and remitted it to the BIR on the payee's behalf.

Here, we’ll explain what the BIR 2307 form is, who needs to issue and receive it, how it must be filed, and (most importantly) how payroll and HR technology like Omni can simplify compliance, turning a potential audit risk into a clear audit trail.

What is the BIR 2307 Form?

The Certificate of Creditable Tax Withheld at Source (BIR Form 2307) is a receipt issued by the payor (the company/withholding agent) to the payee (the contractor/supplier). It documents the income payment that was subjected to Expanded Withholding Tax (EWT) and confirms the exact amount of tax that was already deducted and remitted to the BIR.

In the accounting books of the payee, this form is treated as an asset or an income tax prepayment that will be deducted from their final tax bill.

Differences from the BIR 2316 Form

While both forms certify that tax was withheld, the BIR 2307 and BIR 2316 serve completely different functions and cover different income types. Here’s how they contrast:

Read next: Your Guide to BIR Form 2316

Importance for HR and payroll teams managing contractors

For HR and payroll teams, the accurate issuance and management of the BIR 2307 form is a cornerstone of compliance when dealing with non-employees.

- Audit trail: Issuing the form creates a clear audit trail, demonstrating that the company (as the withholding agent) correctly deducted and remitted the mandated taxes to the government.

- Compliance for payee: It is the official proof that the payee needs to claim the tax credit on their Income Tax Return (ITR); without it, they risk overpaying taxes. HR/Finance must issue it to maintain good vendor relations and compliance.

- Penalty avoidance: Failing to withhold, remit, or issue the BIR Form 2307 correctly can result in significant penalties, surcharges, and interest payments for the business.

Who needs to file the BIR 2307 Form?

The process involves two parties: the withholding agent (the company that issues the form) and the income recipient (the contractor/supplier who receives and files the form).

Businesses paying contractors, professionals, or suppliers

Your business is required to act as the withholding agent and issue the BIR 2307 form every time you pay an independent contractor, supplier, or freelancer subject to creditable withholding tax.

Common transactions that mandate withholding and issuance of the form include payments for:

- Professional services (e.g., freelancers, consultants, IT specialists, bookkeepers, marketing agencies).

- Rentals (commercial or residential property).

- Contractors and subcontractors (e.g., for services like construction, repairs, or maintenance).

- Regular suppliers (specifically, Top Withholding Agents are directed to withhold 2% on services and 1% on goods from regular suppliers).

Freelancers/contractors receiving income

Freelancers, self-employed professionals, and non-individual entities (corporations) who receive income subject to withholding tax are the payees who receive the BIR 2307. This form is critical for them to manage their own tax liability:

- They must attach the form to their Quarterly/Annual Income Tax Return (ITR) to claim the tax credit.

- Without this certificate, they will not be permitted to claim the amount already withheld, potentially leading to overpayment of taxes.

What is the purpose of the BIR 2307 Form?

The BIR 2307 form serves multiple vital functions for both the government and the taxpayer.

Acts as proof of tax withheld from payments

The primary function of the BIR 2307 is to provide official, credible proof that the payor (your company) has already deducted tax from the payment and remitted that amount to the Bureau of Internal Revenue (BIR) on the payee's behalf. This prevents the contractor or supplier from accidentally paying tax twice on the same income.

Can be credited against income tax due

For the payee, the amount indicated on the Form 2307 is recorded as an income tax prepayment in their books. When they file their Quarterly Income Tax Return (Form 1701Q or 1702Q) or Annual Income Tax Return (Form 1701 or 1702), they use the accumulated amount of all received in Form 2307 to offset their final income tax due.

Required for filing quarterly/annual income tax return

The BIR 2307 form is a mandatory attachment for tax filing.

- Income Tax Returns (ITR): The certificate must be attached to the Quarterly/Annual ITR (BIR Forms 1701Q/1701 for individuals or 1702Q/1702 for non-individuals).

- Other taxes: It is also required when filing for Percentage Taxes on Government Money Payments (BIR Form 2551M and 2551Q) and for VAT Withholding (BIR Form 2550M and 2550Q).

Ensures government collection of advance taxes

The entire system of Creditable Withholding Tax (CWT), which the BIR 2307 documents, is designed to allow the government to collect income taxes throughout the year instead of waiting for the annual tax deadline. This system aids in regular revenue collection and helps manage the taxpayer's final tax liability.

What income is covered by the BIR 2307 Form?

BIR Form 2307 applies to income payments subject to CWT under the Philippine tax system. This means it covers payments made by a withholding agent (such as a company or government agency) to individuals or entities for certain goods or services.

Essentially, any payment where the payer is required to withhold a portion of tax on behalf of the payee falls under the coverage of BIR Form 2307.

This form serves as proof that the income earner’s tax was partially prepaid, allowing them to claim it as a tax credit when filing their quarterly or annual income tax return.

How to Fill Out BIR 2307 Form

The responsibility for correctly completing the BIR 2307 form falls on the payor (your company), the withholding agent. Accuracy is paramount, as errors can lead to tax complications for both parties and potential penalties during an audit.

The BIR 2307 form has two main sections that must be completed:

- Part I (Payee Information): This section identifies the income recipient (the contractor/supplier).

- It requires the Payee's Name, Taxpayer Identification Number (TIN), Address, and the period covered by the certificate.

- Part II (Payor Information and Withholding Details): This section identifies your company (the withholding agent) and the transaction details.

- It requires the Payor's Name, TIN, and Address.

- It contains a detailed table (Part II) where you enter the Alphanumeric Tax Code (ATC), the nature of the income payment, the gross amount of income paid, and the rate and amount of tax withheld.

Common mistakes to avoid

- Incorrect ATC: The BIR provides a detailed list of ATCs for different income types. Using the wrong code is a common mistake and can lead to immediate complications for the payee when they file their ITR.

- Miscalculating the tax base: When the payee is VAT-registered, the Expanded Withholding Tax (EWT) should be computed only on the gross amount excluding the 12% VAT. Failure to exclude VAT before computing EWT leads to over-withholding and errors.

- Using the wrong rate: The EWT rate often depends on whether the payee is an individual or corporation, and whether their gross annual income exceeds certain thresholds (e.g., PHP 3 Million or PHP 720,000). If the payee does not provide a sworn declaration of their income level, the payor may be required to use the higher rate.

- Losing VAT status: For VAT-registered payees, the income must be excluded from VAT before EWT calculation.

BIR 2307 Form Filing Process and Deadlines

The issuance and filing of the BIR 2307 form are tied to a series of quarterly and annual deadlines for the withholding agent (your company).

Frequency and deadlines

The payor must issue the BIR 2307 form to the payee based on the following schedule:

- EWT (Expanded Withholding Tax): The certificate must be furnished to the payee on or before the 20th day of the month following the close of the taxable quarter in which the income was earned.

- Example: For payments made in the first quarter (Jan-Mar), the 2307 must be issued by April 20th.

- Upon request: The payor must furnish the statement simultaneously with the income payment if the payee requests it.

- Other taxes: The deadlines vary for other types of withholding:

- Percentage taxes: Issued on or before the 10th day of the month following the month in which withholding was made.

- VAT withholding: Issued on or before the 10th day of the month following the month in which withholding was made.

Who files what (Withholding agent's compliance)

The issuance of the BIR 2307 is only one part of the withholding agent's obligation. Your company must also file the remittance forms for the tax that was withheld:

- Monthly remittance: Use BIR Form 0619E to remit the creditable income tax withheld for the month.

- Quarterly remittance: File BIR Form 1601-EQ (Quarterly Remittance Return of Creditable Income Taxes Withheld). This must be accompanied by the Quarterly Alphalist of Payees (QAP), which details the list of contractors from whom tax was withheld.

- Annual filing: File BIR Form 1604-E (Annual Information Return of Creditable Income Tax Withheld). This form summarizes all EWT payments made during the year and must be accompanied by the annual Alphalist of Payees.

Online vs. manual filing

The BIR has moved towards mandatory electronic submission for many forms, including copies of BIR Form 2307.

- Electronic Filing and Payment System (eFPS): Mandatory for large taxpayers and certain corporations.

- eBIRForms: Used by individual taxpayers and smaller businesses.

- Scanned copies: Taxpayers are now required to submit scanned copies (soft copies) of the original BIR 2307 forms using facilities like the Electronic Audited Financial Statement (eAFS). Hard copies are generally no longer accepted.

Access the eFPS here.

Tax Rates and Withholding for BIR 2307 Form

The BIR Form 2307 serves as proof of CWT deducted at source. It shows that a portion of a payee’s income tax has already been withheld and remitted by the payer to the Bureau of Internal Revenue.

The rates vary depending on the nature of income and the type of payee:

Here are examples of how you might apply those calculations:

Supplier example:

A company pays PHP 100,000 for repair services.

- Repair services are classified as “services” under the TWA rules.

- Withholding tax = PHP 100,000 × 2% = PHP 2,000

- Net payment to supplier = PHP 100,000 - PHP 2,000 = PHP 98,000

Professional services example:

A consultant bills PHP 50,000 for advisory services.

- Advisory or consultancy services fall under “professional fees”.

- Withholding tax = PHP 50,000 × 10% = PHP 5,000

- Net payment = PHP 50,000 - PHP 5,000 = PHP 45,000

The withheld amount is reflected in BIR Form 2307 and can be credited against the payee’s income tax liability when filing their income tax return.

Challenges for Employers Managing BIR 2307 Form

Managing the BIR 2307 form is one of the most meticulous and error-prone compliance duties for HR and finance teams in the Philippines, often leading to audit risks if handled manually.

Manual tracking of payments and tax withheld

Businesses must issue a BIR 2307 every time they pay a contractor subject to Expanded Withholding Tax (EWT). For companies managing multiple contractors and suppliers across various spending categories (professional fees, rentals, services, etc.), manually tracking these individual payments and reconciling the total withheld amount against quarterly remittance forms (BIR Form 1601-EQ) is extremely challenging.

Ensuring timely issuance to contractors

The BIR 2307 must be furnished to the payee on or before the 20th day of the month following the close of the taxable quarter, or immediately upon the payee's request. Missing this deadline can prevent the payee from claiming their tax credit, damaging the company's relationship with its vendors, and potentially leading to the withholding agent's liability for failure to issue the form.

Reconciling multiple contractors and quarterly filings

The BIR uses a stringent TIN-matching validation process, where the amounts reported on the BIR 2307s must perfectly align with the amounts reported on the withholding agent’s Quarterly Alphalist of Payees (QAP) and annual reports (BIR Form 1604-E).

Risk of BIR penalties for non-compliance

The consequences for failure to comply with the proper withholding and documentation requirements are severe:

- Surcharges and interest: Late remittance of the withheld tax is subject to a 25% or 50% surcharge plus 20% annual interest.

- Criminal liability: Failure to deduct, withhold, remit, or issue the BIR 2307 forms can result in fines ranging from PHP 10,000 to PHP 100,000 and even imprisonment.

How Omni Helps with Contractor Management Compliance

Managing contractor payments in the Philippines can be quite tricky given the different deadlines and BIR Form types. With Omni, HR and finance teams can automate the most time-consuming aspects of withholding tax management, BIR Form 2307 generation, and record-keeping, all in a single platform.

Omni provides local compliance with modern software, replacing the need for multiple spreadsheets and scattered systems with a smart, easy-to-use interface that keeps your organization compliant with BIR 2307 Form requirements without the administrative overload.

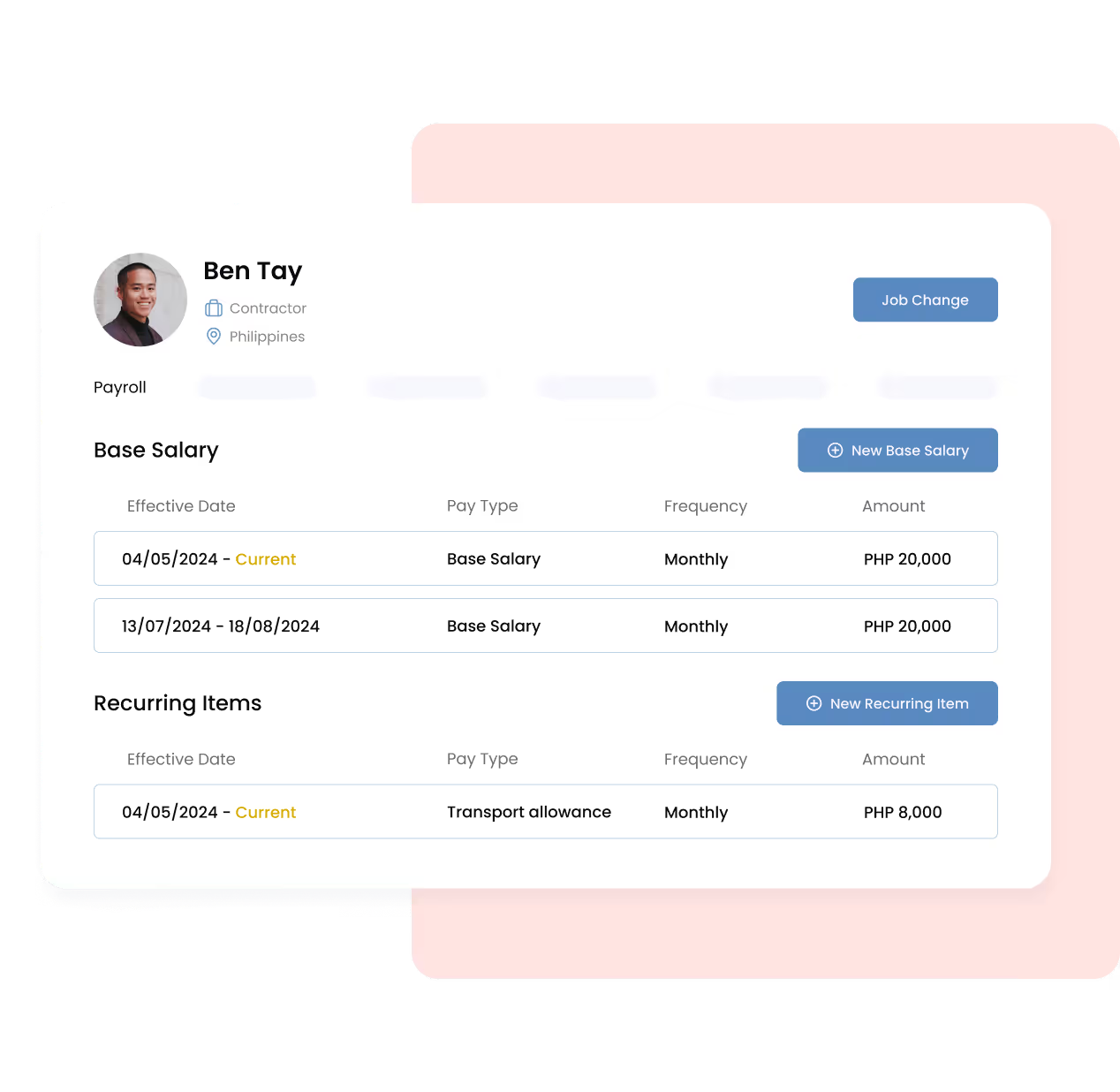

Payroll automation and compliance

Omni’s multi-country payroll solution supports local regulations and statutory contributions in 190+ countries, including the Philippines. Our system automatically applies the correct EWT rates, statutory contributions like SSS, PhilHealth and Pag-IBIG, generates digital certificates, and syncs payment data across your system and employee records, ensuring accuracy each pay run.

Access my free SSS contribution calculator

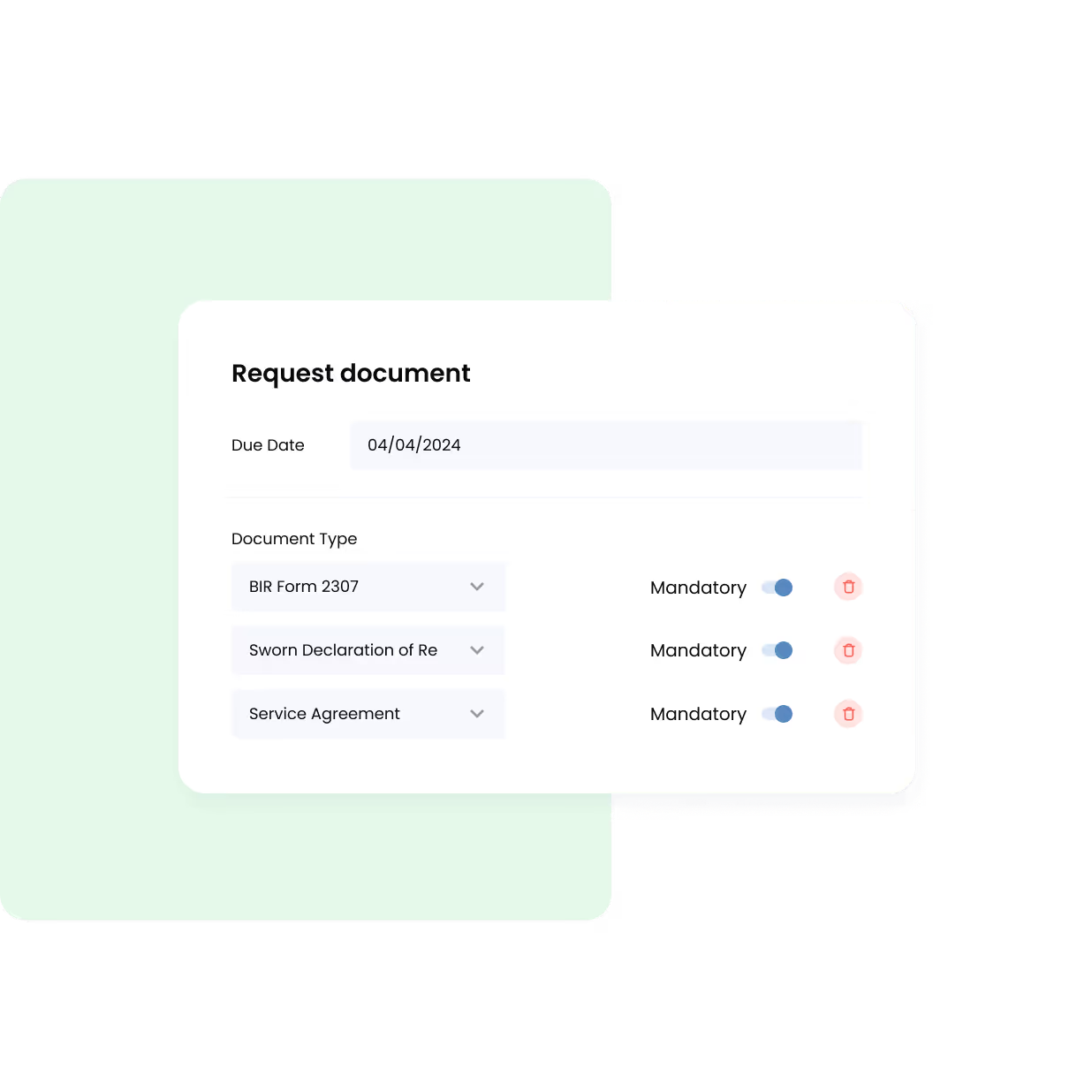

Centralized document and audit trail management

With Omni’s centralized document management and workflow automation, every contractor’s 2307 BIR Form, tax certificate, and transaction record lives in a secure, searchable place. You’ll never lose track of deadlines and important documents during audits again.

Simplified contractor onboarding and self-service

Our custom templates and role-based document access make contractor onboarding and renewal a breeze. Empower your contractors to view payslips, tax forms, and status directly with our self-service portal.

“By having systems like Omni in place, our employees can be more resourceful and know exactly where to find the information they need.”

— Roxanne McGovern, Chief Culture Officer at NightOwl Consulting

Scalable infrastructure for growing teams

From freelancers and subcontractors to multi-country teams, Omni scales with you. Starting at US$3 per employee per month, you get the enterprise-grade HR system that unifies payroll, compliance, and contractor management into one.

Omni gives your HR team the upgrade it deserves, turning manual tax and compliance work into a transparent and automated process. Schedule your product tour today and learn more about Omni’s multi-country payroll.

.png)

.png)