Summary. When a foreign employee or Singapore Permanent Resident (SPR) leaves employment, employers must complete tax clearance by filing Form IR21 with the Inland Revenue Authority of Singapore (IRAS) to ensure all taxes are settled before departure. Late filing, incorrect withholding, or releasing payments before receiving the IRAS Clearance Directive can result in fines of up to S$5,000 or liability for unpaid taxes. Employers must report all income up to the cessation date and file the IR21 form at least one month before the employee’s last working day. Using the IRAS tax clearance calculator and HR systems like Omni’s payroll platform helps automate calculations and reporting, ensuring smooth and compliant tax clearance in Singapore.

When a foreign employee or Singapore Permanent Resident (SPR) leaves your company, the final goodbye involves more than just a farewell party; it triggers a mandatory, time-sensitive compliance event known as tax clearance. This legal obligation requires the employer to file Form IR21 with the Inland Revenue Authority of Singapore (IRAS).

Many HR and payroll decision-makers underestimate the gravity of this process: failing to file the IR21 form on time, miscomputing the amounts to withhold, or releasing final monies prematurely can expose the employer to penalties of up to S$5,000 or even make the company liable for the employee’s unpaid tax.

In this guide, we’ll offer employers a clear, practical roadmap for managing the entire IRAS tax clearance for foreigners process. We’ll cover exactly when the IR21 is needed, detail your key obligations (including complex topics like the "deemed exercise" rule for stock options), highlight common pitfalls, and demonstrate how modern payroll systems like Omni can automate this high-risk compliance area.

What is IR21 and tax clearance in Singapore?

The IR21 is the official tax form submitted by employers to the Inland Revenue Authority of Singapore to notify the authority when a foreign or non-citizen employee ceases employment or leaves Singapore.

- Purpose: The entire tax clearance process is mandatory and serves as a safeguard to ensure that all tax liabilities on the employee's employment income are settled before the individual leaves Singapore or ends their employment.

- Distinction vs. regular tax filing: Unlike the routine annual income tax return (Form IR8A) filed for all employees, IR21 is a one-off clearance process triggered only by specific events involving non-Singapore Citizens (including Foreign Nationals and Singapore Permanent Residents).

When is tax clearance required in Singapore?

As an employer, you have a legal obligation to seek tax clearance by filing Form IR21 for a non-Singapore Citizen employee (Foreign National or SPR) under the following specific scenarios:

Scenarios requiring IR21 tax clearance

- Employee ceases employment: The non-citizen employee is terminating their employment (resignation or termination).

- Employee posted overseas or leaves Singapore for more than three months: The employee is transferred to an overseas office or leaves Singapore for any period exceeding three continuous months. This is required to ensure that the individual's tax residency status and liabilities are correctly managed.

When tax clearance is not required/exemptions

Filing Form IR21 is generally not required in these situations:

- Singapore citizens or PRs not leaving permanently: For Singapore Citizens or PRs who are not leaving Singapore permanently after ceasing employment. (However, if a PR is leaving permanently, tax clearance is required.)

- Short employment period: Non-citizen employees who worked for 60 days or less in a calendar year. (This exemption does not apply to directors or public entertainers.)

- Low income: Non-citizen employees who worked for 183 days or more in a calendar year and earned less than S$21,000 annually.

- Internal transfer: The employee is transferred to another company in Singapore due to a merger, takeover, or restructuring within the same group of companies, provided you notify IRAS via myTax Mail.

Use of the tax clearance calculator by IRAS

IRAS provides a Tax Clearance Calculator to help employers determine quickly if filing IR21 is required for a non-citizen employee based on their circumstances and income levels.

Key Employer Obligations and Withholding Requirements

The moment an employer becomes aware of an impending cessation or departure, a series of critical legal obligations is triggered. These include:

Advance filing/notice

The employer must file Form IR21 at least one month before the employee's final working day or the date of their departure from Singapore, whichever is earlier. Unless there are valid reasons (e.g., immediate resignation), late filing may result in a fine of up to S$5,000.

Withholding of monies due to the employee

- The requirement: You are required to withhold all monies due to the employee from the date you are made aware of their impending cessation of employment or departure. This includes all forms of compensation: salary, bonuses, overtime pay, leave pay, allowances, gratuities, and lump sum payments.

- When to release: These withheld funds cannot be released until you receive a clearance directive from IRAS.

If the employer is unable to withhold

If you are unable to withhold all monies due to the employee, you must provide IRAS with the reason in Form IR21. Failure to withhold the required monies without a valid reason could leave your organization liable for the employee’s owed tax.

Reporting all income up to the cessation date

In Form IR21, you must report the employee's total income earned up to the date of cessation or departure. This includes the income earned in the current year, as well as any income from the preceding year that was not already transmitted electronically via the Auto-Inclusion Scheme (AIS).

Special cases: deemed exercise rule for ESOPS

A special rule applies to employee stock options (ESOPs) and share awards that are unexercised or unvested at the time of departure. Under the "deemed exercise" rule, the employee is considered to have derived gains from these options or awards at the point of tax clearance, and these gains must be included as taxable income in the IR21 submission.

Penalties for late or non-filing

Employers who fail to file Form IR21 or file it late may be liable to a fine of up to S$5,000. Additional penalties may apply for under-reporting income or releasing funds prematurely.

How to Fill and Submit IR21

The fastest and most reliable method for tax clearance is electronic filing, though paper filing is still a viable option. Here’s how each works:

Mode of Filing: E-filing or Paper Filing

- e-Filing: Submission through the IRAS myTax Portal is encouraged. E-filed forms are typically processed within 7 working days.

- Paper Filing: Submission via hard copy takes longer, typically within 21 days.

Appendices to attach

Depending on the income type, specific appendices must be completed and e-filed with Form IR21:

- Appendix 1: For the value of benefits-in-kind provided.

- Appendix 2: For details of gains/profits from exercised/deemed exercised ESOPs/ESOW plans for the year.

- Appendix 3: For details of unexercised or restricted ESOPs/ESOW plans that are tracked by the employer as of the cessation date.

Checking and withdrawing IR21

Employers can check the status of tax clearance and view the Clearance Directive online via the myTax Portal. If changes are needed to the income details originally submitted, an Amended Form IR21 must be filed. If only the amount of money withheld needs to be changed, IRAS should be informed via email instead of filing an amended form.

Tax Clearance Processing, Outcome, and Payment for IR21

Processing time

The processing time for e-filed forms is generally within 7 working days, whereas paper filing takes up to 21 days. Delays may occur if information is incomplete or clarification is needed.

Clearance directive options

Once the tax liability is determined, IRAS sends a Clearance Directive to the employer:

- Directive to pay tax: This notifies the employer of the exact tax amount to be remitted to IRAS.

- Notification to release monies: This directs the employer to release the withheld balance to the employee (if the tax due was less than the amount withheld).

When to pay clearance tax

The employer is required to pay the amount of tax stated in the Directive to Pay Tax to IRAS within 10 days from the date of the Directive.

Refunds

If the amount of money the employer withheld from the employee is more than the final tax assessed by IRAS, the employer must release the balance (the refund) to the employee upon receiving the Clearance Directive.

Common IR21 Challenges and Pitfalls

HR and payroll teams often face difficulties that can lead to non-compliance:

- Missing the one-month notice/late filing: This is the most common error, and late filing can lead to fines.

- Under-reporting income: Forgetting to include certain benefits-in-kind, bonuses, or, critically, gains from stock options (due to the deemed exercise rule) exposes the employer to liability.

- Incorrect withholding or releasing funds prematurely: Releasing any part of the final payment before receiving the IRAS Clearance Directive is a violation, making the employer liable for any outstanding tax.

- Failing to attach the correct appendices: Incorrect or missing attachments (especially for share scheme gains) prolong the processing time and can delay tax clearance.

- Reconciliation between payroll records and IRAS records: Mismatched employee income figures between the company's payroll system and IRAS records often cause delays and require time-consuming manual reconciliation.

Frequently Asked Questions

1. When must an employer file Form IR21 for an employee?

The employer must file Form IR21 at least one month before the earliest of the following dates

- The employee ceases to work for the employer in Singapore (resignation or termination).

- The employee starts an overseas posting.

- The employee leaves Singapore for any period exceeding three continuous months.

If the employer is unable to give one month’s notice, for instance, due to an immediate resignation, a valid reason must be provided in the IR21 Form submission. Timely filing helps ensure smooth tax clearance in Singapore and avoids penalties.

2. Are Singapore citizens or non-resident employees required to have IR21 tax clearance?

Singapore citizens: No, tax clearance is generally not required for Singapore Citizens.

Non-citizen employees: Yes, tax clearance is mandatory for all non-citizen employees, which includes foreign nationals and Singapore Permanent Residents (SPRs) who are:

- Ceasing employment

- Posted overseas

- Leaving Singapore permanently

SPRs who are not leaving Singapore permanently can be exempted from filing Form IR21 if they provide a Letter of Undertaking (LOU) to their employer.

There are also specific IRAS tax clearance exemptions for employees who:

- Worked in Singapore for 60 days or less,

- Earned less than S$21,000 in the preceding year, or

- Have been employed continuously for at least 3 years and earn less than S$21,000 annually.

These exemptions apply only to certain categories of non-citizen employees, so employers should always verify using the IRAS tax clearance calculator.

3. What types of income should be included in IR21 (bonuses, stock options, benefits)?

Employers must report all income earned by the employee up to the date of cessation or departure in the IR21 Form. This includes:

- Salary and lump sum payments: Basic salary, bonuses, overtime pay, leave pay, and gratuities.

- Benefits-in-kind: Non-cash benefits, such as housing provided by the employer

- Share gains: Gains from the "deemed exercise" of unexercised/unvested stock options or share awards.

- Preceding year income: Income earned in the preceding year that was not previously reported to IRAS via the Auto-Inclusion Scheme (AIS).

Ensuring accurate reporting of all taxable income helps IRAS compute the correct tax clearance amount and avoid discrepancies during assessment.

4. Can Form IR21 be filed late or amended?

Late filing: Employers can submit the IR21 Form late only with a valid reason (e.g., immediate resignation). Filing late without reasonable cause may result in a fine of up to S$5,000 under IRAS regulations.

Amended filing: Employers must file an Amended Form IR21 if errors or updates are discovered after the initial submission. However, if the only change relates to the amount of money withheld for tax clearance, employers may notify IRAS via email instead of filing a new form.

Keeping accurate records and submitting on time helps streamline the tax clearance process in Singapore.

5. What is the processing time for tax clearance via IR21?

Processing time depends on the submission method used:

- e-Filing (via myTax Portal): Typically processed within 7 working days.

- Paper Filing: Typically processed within 21 days.

IRAS may take longer if the Form IR21 submission is incomplete or requires clarification. Employers can check the status of their IR21 tax clearance on the myTax Portal.

6. What happens if I release monies before clearance?

Employers are legally required to withhold all monies due to the employee (including salary and bonuses) until the IRAS Clearance Directive is received.

If an employer releases payment before receiving the directive, they may be held personally liable for any outstanding tax clearance amount owed by the employee. Always ensure clearance is received before releasing final payments.

7. How is the “deemed exercise” of shares handled in IR21?

Under the “deemed exercise” rule, any unexercised Employee Stock Options (ESOPs) or unvested Employee Share Ownership (ESOWs) held by the employee are treated as if they were exercised or vested on the last day of employment or departure.

The employer must calculate the gains from this "deemed exercise" and include them as part of the employee’s taxable income in the Form IR21 submission. The details of these unexercised or unvested shares should be reported in Appendix 3, attached to the IR21 form.

Employers can use an IR21 calculator, consult IRAS guidance, or use HR software built for Singapore to compute the taxable gains from share options accurately.

How Omni Helps with IR21 Clearance

When dealing with tax clearance in Singapore, it goes beyond just submitting Form IR21. Employers must ensure precision, local expertise, and data coordination across payroll, employee records, and compliance workflows. Manual tracking or legacy systems can easily lead to delays, inaccurate reporting, or missed deadlines.

Omni’s all-in-one HR platform transforms this risky compliance process into a smooth, automated workflow. Here’s how:

Automate local compliance

Built specifically for growing teams in Singapore and Asia, Omni makes local statutory compliance simple, from automated payroll and statutory calculations to accurate IR21 tax clearance reporting.

Our integrated employee database empowers HR teams to pull accurate information on salary, benefits, and stock options without jumping between disparate systems.

“Omni provided us with a unified platform that integrates all essential HR functions—from employee profiles and performance management to leave tracking and payroll—all in one accessible location.”

— Wenna Lee, HR Manager at IHRP

Simplify document collection and tracking

With secure document management, employers can easily store and retrieve documents like employment contracts, work permits, and stock option details for IR21 tax clearance filings.

HR managers can set reminders with automated workflows to ensure no expiry or documents are missed.

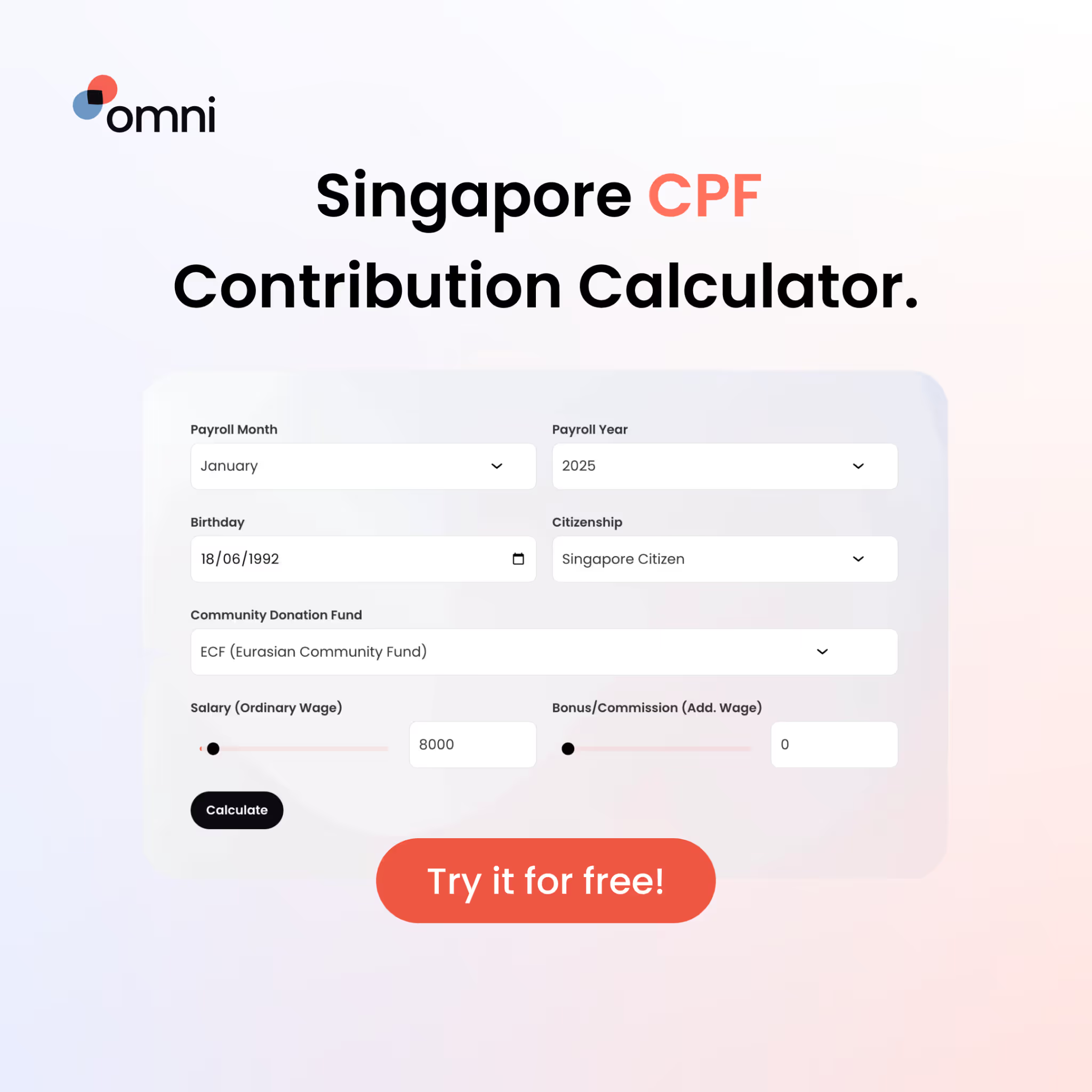

Payroll system built for Singapore

Omni’s localized payroll feature automates the computation of all final payments and tax deductions in line with Singapore’s IRAS requirements. With specific statutory calculators like CPF and instant payroll reports, HR teams can ensure accuracy and compliance in every tax clearance Singapore submission.

Our payroll integrates directly with time-tracking and accounting systems like Xero, making it easy to confirm total income up to the cessation date, including bonuses, benefits-in-kind, and taxable share gains.

“Payroll calculations that used to take three to five working days can now be done in half the time with Omni.”

— Tengku Mohaizad, Group Head of HR Asia at Inspire Brands Asia

Local support whenever you need it

Omni’s award-winning local support team operates within APAC time zones, ensuring real-time help with IR21 form submissions, payroll configuration, and IRAS tax clearance queries.

“The support from Omni over Slack has been fantastic. Having the team right here in the region means they understand our needs and can respond quickly.”

— Derek Tan, Head of HR at Milieu Insight

Schedule your product tour and streamline your tax clearance process with Omni today.

.png)

.png)