Summary. CPF employer contribution is one of the most compliance-sensitive obligations a Singapore employer manages — and one of the most error-prone when handled manually. Contribution rates vary by employee age, salary, and citizenship status. PR employees follow a graduated schedule that changes twice before reaching full rates. Ordinary Wage and Additional Wage ceilings cap how much of an employee's income is CPF-payable, and those caps updated again in January 2026. This guide covers what employers need to get right, the mistakes that most commonly trigger CPF Board audits, and how modern payroll software removes the manual overhead entirely.

What is CPF Employer Contribution?

CPF employer contribution is the mandatory monthly payment Singapore employers make to every eligible employee's Central Provident Fund (CPF) account. Alongside the employee's own contribution, the employer's share is calculated as a percentage of the employee's wages — with rates that vary based on the employee's age bracket, citizenship status (Singapore citizen vs Permanent Resident), and how long a PR employee has held that status.

For most Singapore citizens aged 55 and below, the combined CPF contribution rate is 37% of monthly wages — 17% from the employer and 20% from the employee. Those rates step down progressively as employees pass age thresholds at 55, 60, 65, and 70.

Getting CPF employer contributions wrong — even systematically, even by small amounts — carries real consequences. The CPF Board charges interest on late or underpaid contributions, and repeated errors can trigger formal audits. For most HR teams, the risk isn't a single large mistake. It's small, compounding errors from manual calculations, missed birthday-triggered rate changes, or incorrect PR contribution phases that accumulate across months before anyone catches them.

CPF Contribution Rates by Age Bracket

CPF contribution rates in Singapore are tiered by age, with separate rates for employer and employee contributions. From 1 January 2026, the rates for Singapore citizens and third-year-and-beyond PRs are:

Rate changes take effect in the employee's birthday month — not at the start of the calendar year and not at the start of the next payroll cycle. Missing a birthday-triggered transition is one of the most common CPF compliance errors. Payroll software that auto-detects upcoming age-bracket changes and applies the new rates in the correct month removes this risk entirely.

For the most current contribution rate tables including the January 2026 updates, see the CPF Board's employer rates page.

CPF Ordinary Wage Ceiling and Additional Wage Ceiling

What is the CPF Ordinary Wage (OW) Ceiling?

The Ordinary Wage ceiling is the maximum monthly salary on which CPF contributions are calculated. From 1 January 2026, the OW ceiling is S$8,000 per month (increased from S$7,400). This means that for an employee earning S$10,000 per month, CPF contributions are only calculated on the first S$8,000 — the remaining S$2,000 is not CPF-payable.

The OW ceiling increase from S$7,400 to S$8,000 took effect on 1 January 2026. If your payroll system hasn't been updated to reflect this change, your CPF calculations have been incorrect since January.

What is the CPF Additional Wage (AW) Ceiling?

Additional Wages — bonuses, commissions, and other variable payments that are not paid monthly — are subject to a separate annual cap. The AW ceiling for CPF purposes is S$102,000 minus the total Ordinary Wages already subject to CPF that calendar year.

In practice: an employee earning S$8,000/month has S$96,000 of CPF-liable OW by year-end (12 × S$8,000). Their AW ceiling is therefore S$102,000 − S$96,000 = S$6,000 for the year. CPF is only calculated on bonuses up to that remaining cap, regardless of how large the bonus actually is.

Confusing the monthly OW ceiling with the annual AW ceiling is among the most common sources of payroll miscalculation — particularly at year-end when annual bonuses are processed.

CPF Contributions for Permanent Residents

Singapore Permanent Residents do not contribute at full citizen rates immediately. They follow a graduated contribution schedule for their first two years of PR status, with reduced rates for both the employer and employee before transitioning to full rates in their third year.

The graduated schedule exists to ease the cost of CPF contributions for newly permanent residents during the transition period. The specific rates differ by year-of-PR status and age bracket — for a full breakdown, see our dedicated PR CPF contribution rates guide.

From a payroll compliance perspective, the most common PR-related errors are:

- Applying the wrong tier — failing to track when an employee transitions from Year 1 to Year 2, or Year 2 to full rates

- Using the PR start date incorrectly — the graduated schedule runs from the date the employee obtained PR status, not their employment start date with your company

- Missing the transition to full rates — employees in their third year of PR status should contribute at full citizen-equivalent rates, but manual systems often fail to catch this without a triggered alert

A payroll system that tracks each employee's PR start date, detects phase transitions automatically, and applies the correct graduated rates removes all three error sources.

Skills Development Levy (SDL)

What is SDL?

The Skills Development Levy is a mandatory contribution paid by all Singapore employers for employees earning S$800 or less per month. The levy rate is 0.25% of the employee's gross monthly wages, capped at S$11.25 per employee per month. SDL is collected by the CPF Board alongside CPF contributions and funds Singapore's SkillsFuture workforce training programmes.

SDL applies to all employees — full-time, part-time, casual, and foreign workers — as long as their gross monthly wages do not exceed S$800. For employees earning above S$800, SDL still applies at the minimum levy of S$2.

SDL is a small levy but easy to overlook for businesses new to Singapore payroll, particularly when managing a mix of full-time and part-time staff. Modern payroll software calculates SDL automatically alongside CPF contributions in each payroll run, so it never requires a separate calculation.

IRAS AIS and IR8A: Annual Filing Requirements

Auto-Inclusion Scheme (AIS)

The Inland Revenue Authority of Singapore (IRAS) requires employers with six or more employees to participate in the Auto-Inclusion Scheme (AIS). Under AIS, employers must submit employment income information for all employees electronically by 1 March each year.

AIS participation means IRAS pre-populates employees' personal income tax returns with the employer-submitted data — making filing easier for employees and removing the need to submit paper IR8A forms directly to employees.

What is IR8A?

IR8A is the annual return of employee earnings that Singapore employers must prepare for every employee. It captures total wages, bonuses, allowances, and other remuneration for the calendar year. For employers on AIS, IR8A data is submitted electronically to IRAS rather than issued as a paper form to employees.

Employers not on AIS (fewer than six employees) must issue the physical IR8A to employees by 1 March so they can file their own tax returns.

Relevant appendices include IR8S (for employers who have made excess CPF contributions), Appendix 8A (for benefits-in-kind), and Appendix 8B (for gains from share options).

Payroll software should auto-generate IR8A forms and the relevant appendices, and support direct AIS e-filing submission to IRAS. Assembling these manually at year-end is a significant compliance risk and unnecessary administrative burden.

Common CPF Payroll Mistakes That Trigger Audits

Misapplying the OW and AW ceilings

The monthly OW ceiling and the annual AW ceiling serve different purposes and are easily confused. Applying the S$8,000 monthly OW ceiling to a year-end bonus (which is AW subject to its own cumulative cap) is a common error — as is applying the annual AW ceiling calculation incorrectly when an employee receives multiple variable payments throughout the year.

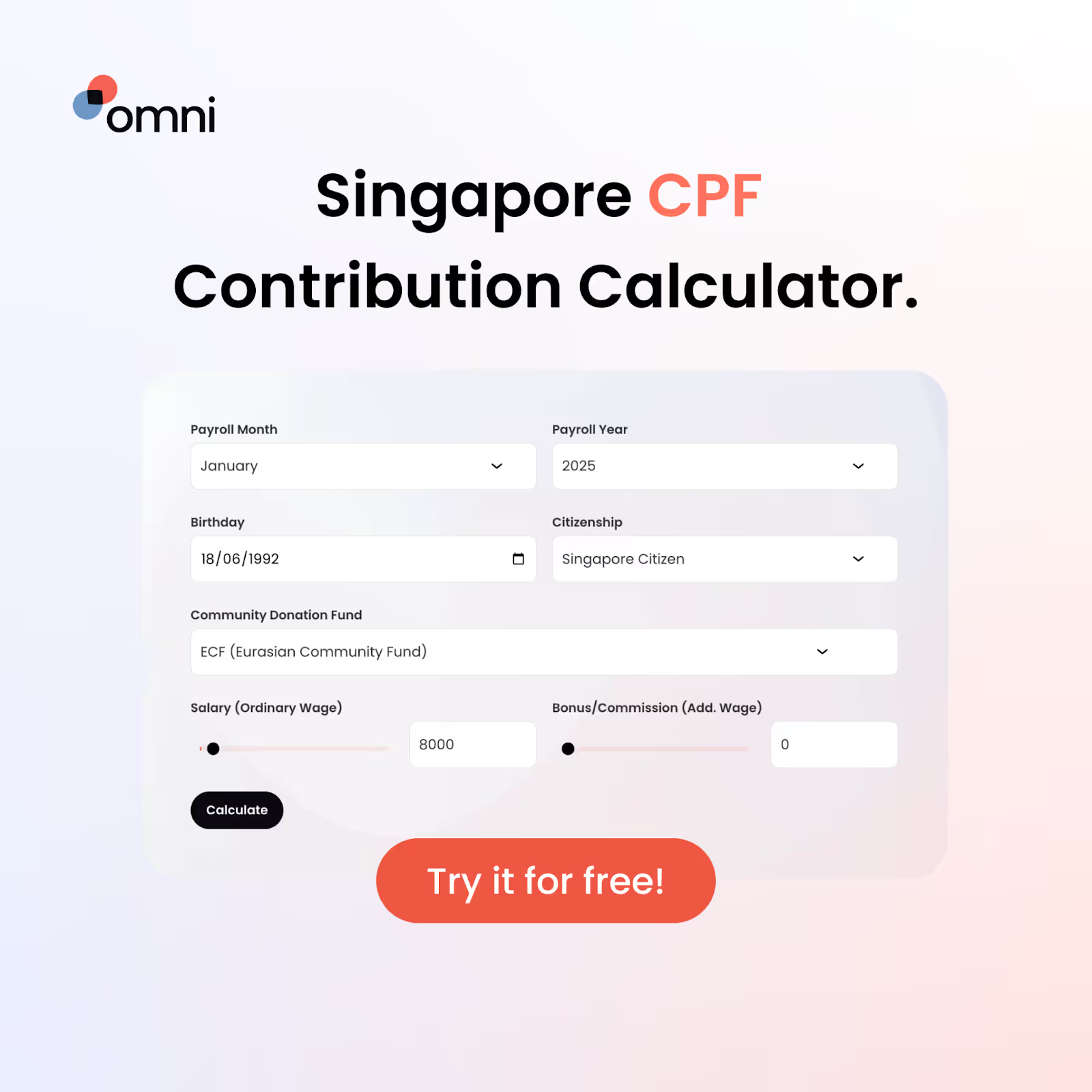

Calculate CPF contributions with our free CPF Calculator

Missing birthday-triggered rate changes

CPF contribution rates step down when an employee crosses an age threshold. These transitions take effect in the birthday month, not at the start of the new year. Without automated tracking, an employee who turns 56 in March will often be calculated at the under-55 rate through to the following January — months of incorrect contributions that need retroactive correction.

Incorrect PR graduated contributions

Applying the wrong contribution tier for PR employees — particularly missing the transition from Year 2 graduated rates to full rates in Year 3 — is a frequent source of underpayment. Errors also occur when the PR start date is recorded incorrectly in the payroll system, shifting the phase transitions by months or years.

Late or missing CPF submissions

CPF contributions are due by the last day of each month, with a grace period to the 14th of the following month (or the next business day if the 14th falls on a weekend or public holiday). Late payments attract interest charges from the CPF Board — currently 1.5% per month on outstanding amounts. Persistent late submission can escalate to formal enforcement action.

How Omni HR Manages CPF Employer Contributions

Unlike legacy payroll tools that require manual rate table updates when regulations change, Omni's payroll engine is built to handle Singapore's CPF complexity automatically.

Built-in CPF compliance:

- Country-specific statutory calculations for Singapore payroll, updated when rates change

- Automatic application of CPF contribution rates and OW/AW ceiling tracking per employee per month

- PR employee profiles that support correct graduated contribution handling — Year 1, Year 2, and full-rate transitions tracked automatically

- Age-bracket monitoring with automatic rate changes applied in the correct birthday month

- Payroll calculations synchronized with centralized employee and attendance records, so wage components feed directly into CPF calculations without manual re-entry

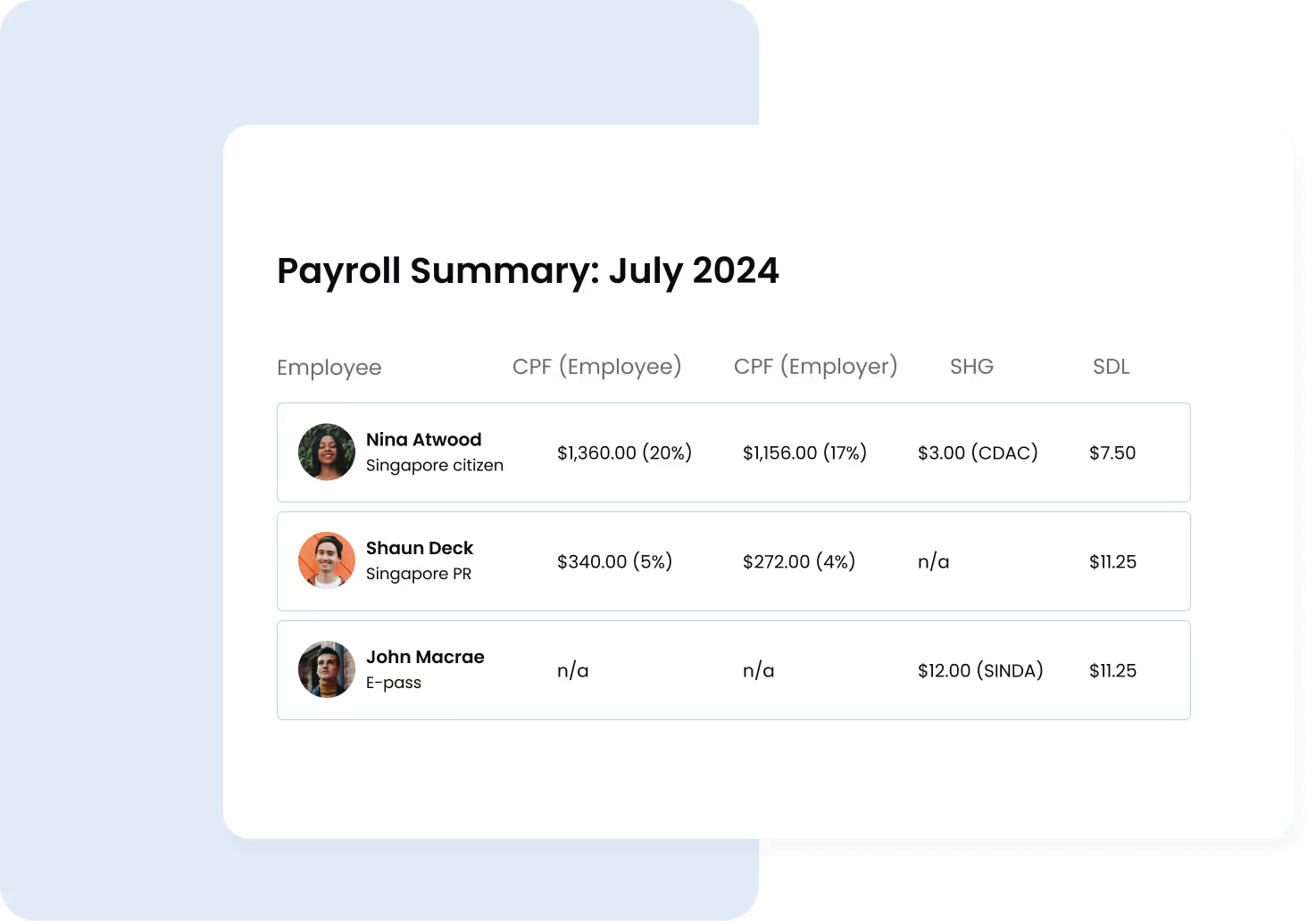

SDL and other statutory payments:SDL, IRAS AIS submissions, and CPF all run through the same payroll workflow in Omni — not as separate processes requiring separate data inputs. This eliminates the reconciliation errors that come from managing statutory payments across disconnected systems.

Audit-ready reporting:

- Instant CPF contribution statements for each employee, showing wage components, contribution timelines, and monthly calculations

- Export-ready statutory documentation for IR8A and AIS submissions

- Customizable payroll reports for internal review and external compliance verification

- Dedicated local APAC support team operating in your timezone

"Payroll calculations that used to take three to five working days can now be done in half the time with Omni."— Tengku Mohaizad, Group Head of HR Asia, Inspire Brands Asia

"Having a single source of truth has improved the accuracy of our data and reporting."— Shux M., Chief People Officer, Endowus

"The support from Omni over Slack has been fantastic. Having the team right here in the region means they understand our needs and can respond quickly."— Derek Tan, Head of HR, Milieu Insight

For a comparison of payroll software platforms that handle CPF compliance automatically, see our Singapore payroll software guide.

Manual vs Legacy vs Omni HR: CPF Payroll Compliance Compared

Related reading:

Frequently Asked Questions

Singapore Permanent Residents follow a graduated CPF contribution schedule for their first two years of PR status, contributing at lower rates before transitioning to full citizen-equivalent rates in their third year. Good payroll software tracks each employee's PR start date, detects when they enter a new contribution phase, and automatically applies the correct rates — without requiring HR to manually update contribution settings. For more detail on how this works, see our CPF management guide.

Yes — the leading Singapore HR software platforms, including Omni, Swingvy, and Payboy, calculate CPF contributions automatically based on employee age band and salary ceiling, and update their engines when MOM adjusts contribution rates. This removes one of the most common sources of payroll error for Singapore businesses.

For Singapore citizens and third-year-and-beyond PRs aged 55 and below, the employer CPF contribution rate is 17% of the employee's monthly wages — giving a combined employer-employee rate of 37%. Rates decrease as employees pass the age thresholds at 55, 60, 65, and 70. Contributions are only calculated on wages up to the Ordinary Wage ceiling of S$8,000 per month (from 1 January 2026). For a full rate table broken down by age bracket, see the CPF Board employer rates page.

From 1 January 2026, the CPF contribution rate for employees aged 55 and below remains 37% combined (17% employer, 20% employee). The main change taking effect in 2026 is the Ordinary Wage ceiling increase from S$7,400 to S$8,000 per month. Senior worker rates above age 55 also saw increases phased in from 2022 through 2026 — see the CPF Board's 2026 contribution changes page for the full schedule.

Ordinary Wages (OW) are the fixed monthly salary an employee receives — subject to a monthly CPF ceiling of S$8,000 from January 2026. Additional Wages (AW) are non-monthly payments like bonuses and commissions — subject to an annual cap calculated as S$102,000 minus the total OW already subject to CPF that calendar year. The distinction matters because the two ceilings apply independently, and applying the wrong ceiling to a bonus payment is a common source of CPF miscalculation.

IR8A is the annual return of employee earnings that Singapore employers must prepare for every employee, capturing total wages, bonuses, allowances, and other remuneration for the calendar year. Employers with six or more employees must submit IR8A data electronically to IRAS via the Auto-Inclusion Scheme (AIS) by 1 March each year. Employers with fewer than six employees must issue the physical IR8A form to each employee by the same date so they can include it in their personal tax filing. Payroll software that auto-generates IR8A and supports AIS e-filing makes year-end compliance significantly faster.

The Skills Development Levy (SDL) is a mandatory levy paid by all Singapore employers for employees earning S$800 or less per month. The rate is 0.25% of gross monthly wages, capped at S$11.25 per employee per month. For employees earning above S$800, a minimum levy of S$2 applies. SDL is collected by the CPF Board alongside CPF contributions. It funds Singapore's SkillsFuture training programmes.

CPF contributions are due by the last day of each month, with a grace period to the 14th of the following month. Late payments attract interest charges of 1.5% per month on the outstanding amount. Persistent non-compliance can escalate to enforcement proceedings by the CPF Board, including court action. Employees are also affected — late contributions reduce their retirement savings for the months involved.

.png)

.png)