Summary. In the Philippines, 13th-month pay is a mandatory benefit under Presidential Decree No. 851, requiring employers to provide rank-and-file employees with an additional payment equal to one-twelfth (1/12) of their basic annual salary. All employees who have worked at least one month—whether full-time, part-time, or probationary—are entitled to it, and it must be released on or before 24 December. Employers must know how to compute 13th-month pay correctly by including only basic salary and excluding allowances or overtime pay. While 13th-month pay and other bonuses are tax-free up to PHP 90,000 under the TRAIN Law, any amount exceeding that limit becomes taxable income. Accurate 13th-month pay computation and timely release are crucial to stay compliant with DOLE regulations and avoid penalties or employee disputes.

In the Philippines, the 13th-month pay is a mandatory benefit that employers must provide to eligible employees under the Presidential Decree No. 851. It’s essentially an extra month’s salary paid out at year-end; it goes from being a bonus to being a legal obligation.

Businesses need to ensure accurate computation and timely release of this benefit to stay compliant and avoid disputes.

In this guide, we’ll explain what 13th-month pay is, who should receive it, when it’s due, how to compute it correctly (with examples), tax implications, and common scenarios.

What is 13th-month pay?

A 13th-month pay is a mandatory employee benefit that serves as an additional payment based on an employee’s basic salary. It is typically equivalent to one-twelfth (1/12) of an employee’s total basic salary earned within a calendar year.

Rather than being a bonus or a performance-based pay, the 13th-month pay is a statutory benefit designed to provide employees with additional financial support at the end of the year.

This is calculated based on the employee's basic pay, which is their usual salary for time worked and paid leaves, and does not take into consideration any additional benefits such as overtime, allowances, or bonuses.

Under the law, all rank-and-file employees in the private sector who have worked for at least one month are entitled to this benefit, regardless of employment status (whether full-time, part-time, probationary, or project-based). The coverage law was later expanded in the late 1980s to remove salary ceilings and subsequently extended under the Kasambahay Law to include household workers.

Who is entitled to 13th-month pay?

The 13th-month pay applies mainly to rank-and-file employees in the private sector who’ve worked at least one month during the year. It doesn’t matter if they’re regular, probationary, project-based, seasonal, or part-time, as long as there’s an employer-employee relationship and they’ve earned basic pay, they’re covered.

Included:

- Rank-and-file employees in private companies, regardless of how they’re paid (monthly, weekly, or daily).

- Those who’ve worked even a portion of the year — their 13th-month pay will simply be prorated.

Excluded:

- Managers and executives, anyone with the power to hire, fire, or make company-wide policy decisions.

- Freelancers, consultants, and independent contractors since they operate under service contracts and aren’t on the company payroll.

- Purely commission-based or boundary-based workers, for example, real estate agents or drivers who earn only from commissions or boundaries. However, if a worker has a fixed basic pay plus commissions, only the basic pay is counted.

- Government employees receive a separate year-end bonus under civil service rules.

Note: Household workers (kasambahays) are also entitled under the Kasambahay Law (RA 10361), with payment due on or before the year ends.

When is 13th-month pay distributed?

Employers have the legal obligation to issue the 13th-month payment on or before 24 December each year as required by the DOLE. Any payment after this date is considered non-compliant and may result in penalties and employee dissatisfaction..

Some companies may opt to divide the payout into two payments, with the first half paid in the middle of the year (around June or July), and the second half paid before 24 December. This arrangement is compliant as long as the entire sum is paid before the due date. Paying in instalments provides employees with better control over their spending and enables businesses to distribute their cash flow more evenly.

How to compute 13th-month pay?

The formula for computing 13th-month pay is simple:

13th-month pay = total basic salary earned during the year / 12

Use our free calculator below for an instant, prorated figure, or follow the manual computation below.

What counts as basic salary?

Only standard wages, paid leaves (approved vacation and sick leave) are counted. These form a part of the regular compensation of the employee.

Note: SSS contributions are deducted before the 13th-month base is calculated. Use our free SSS Contribution Calculator to confirm your exact deduction amount before running the numbers above.

What's excluded?

- Allowances

- Overtime pay

- Holiday allowances

- Night-shift differentials

- Cash value of unused leave

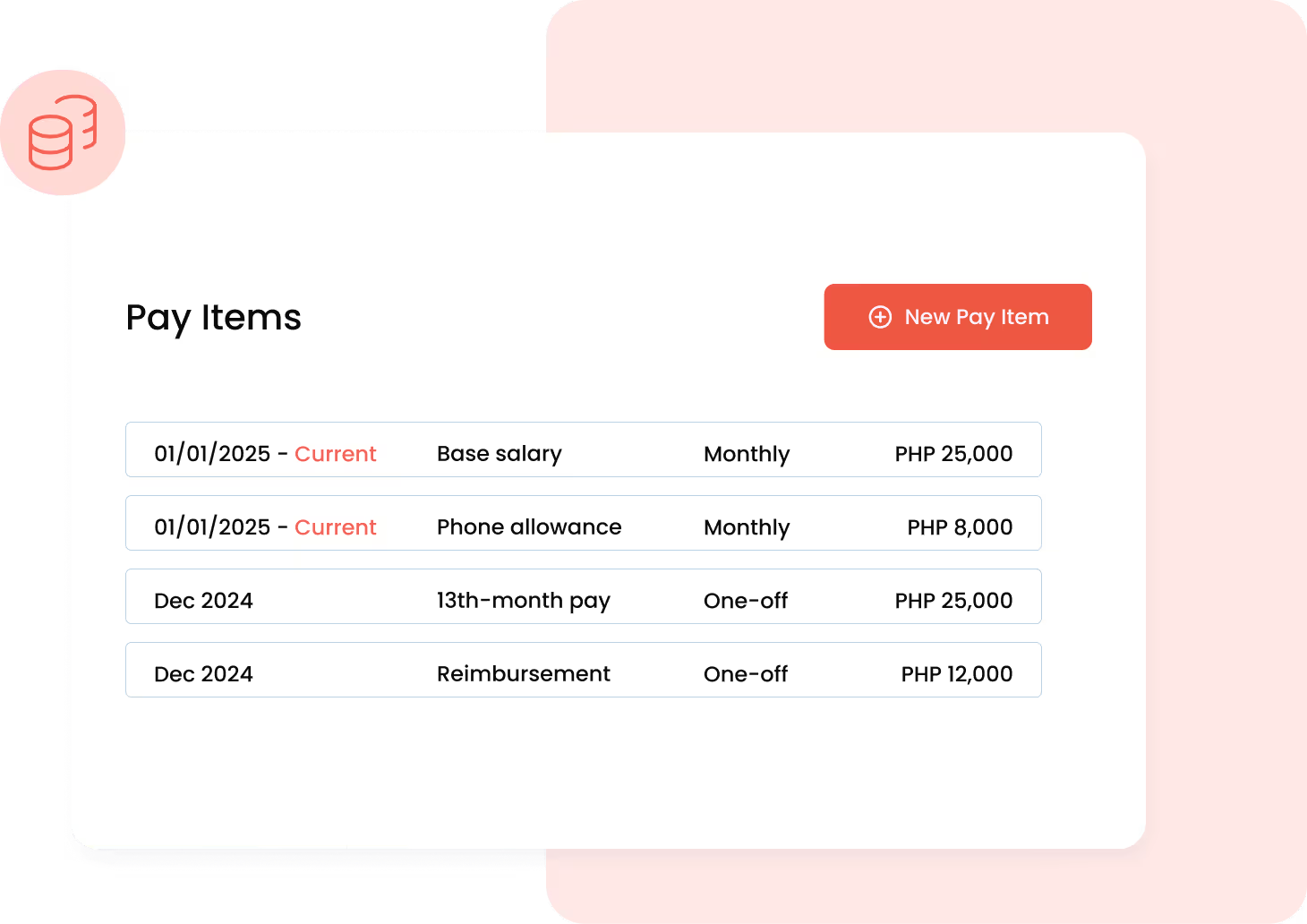

Worked examples

Full-year employee

Mari earns PHP 25,000 a month with no unpaid absences in the year.

- Annual basic salary: PHP 25,000 × 12 = PHP 300,000

- 13th-month pay: PHP 300,000 ÷ 12 = PHP 25,000

Prorated for a mid-year hire

Alon joined in July, earning PHP 20,000 a month, and worked six months (July to December).

- Total basic salary: PHP 20,000 × 6 = PHP 120,000

- 13th-month pay: PHP 120,000 ÷ 12 = PHP 10,000

For businesses managing several employees, this calculation can run automatically with a payroll system like Omni HR, which accounts for paid leave, start dates, and prorated months so the figure stays accurate and compliant without spreadsheets.

Read next: How to Compute Overtime Pay in the Philippines

Is 13th-month pay taxable?

13th-month pay may be taxable depending on your employee’s total yearly bonuses. If bonuses exceed the tax-exempt limit, the excess will be taxable.

Under the TRAIN Law, 13th-month pay and other bonuses are tax-free up to PHP 90,000. When the total bonuses (with the 13th-month pay) of employees remain less than PHP 90,000, no withholding tax applies. However, any amount exceeding PHP 90,000 is taxed as regular income.

For example, Mia receives PHP 70,000 as her 13th-month pay. Since it’s below the limit, it’s fully tax-exempt. On the other hand, Paolo gets PHP 100,000 as his 13th-month pay; the PHP 10,000 excess over the PHP 90,000 threshold will be subject to income tax.

Where payroll teams often get caught off guard is in tracking the combined value of all bonuses across the year, not just the December payout. Mid-year performance bonus and previous incentives within the year must be included towards the PHP 90,000 tax limit. Missing these figures can throw your tax computation off.

Omni’s payroll module makes this part effortless. Built specifically for growing teams in the Philippines, our system automatically tracks employees’ 13th-month pay and bonuses throughout the year, highlighting when employees exceed the PHP 90,000 tax-free limit under the TRAIN Law, and applies the correct tax only to the excess, all without the need for manual spreadsheets and calculations.

"Omni allows us to extract accurate data, which makes it a great platform for timekeeping and payroll."

— Iron Mike Minguez, HR Admin Assistant at Dev Team

Paired with smart workflows, audit-ready reports, and centralized employee records, Omni ensures your payroll stays up-to-date and compliant across every pay cycle.

Common Scenarios in 13th Month Pay Computation

Here’s how to handle the usual edge cases HR teams deal with:

- New hires: Employees who join mid-year are still entitled to 13th-month pay, but it is prorated based on the number of months worked.

- Resigned or terminated employees: They’re entitled to a prorated share of the 13th-month pay computation up to their last working day, usually included in their final pay.

- Probationary staff: Covered just like regular employees, as long as they’ve worked at least a month.

- Employees with variable pay: Only the fixed or guaranteed portion of their income counts. Commissions are included only if defined as part of their basic salary.

- Maternity leave: Days covered by SSS benefits aren’t included, but paid leave days before or after maternity leave still count toward 13th-month pay computation.

- Unpaid leave or no-work-no-pay months: These periods simply reduce the total earnings used in the 13th-month pay computation.

Compliance Risks & Employer Obligations

When it comes to 13th-month pay, the real risk isn’t just missing the payout; it’s getting flagged for non-compliance. DOLE takes this seriously as late release, underpayment, or failure to report can lead to fines, employee complaints, and mandatory corrective actions. All these can affect your company’s standing if DOLE conducts an audit or inspection.

Practically, employers ought to schedule 13th-month compensation alongside routine payroll. This means planning and confirming employee eligibility before processing payments to prevent hasty mistakes. Another best practice is to communicate proactively with staff, informing them of the release date, how their 13th-month pay is calculated, and what to expect if it is prorated. Clear communication reduces confusion and ensures transparency.

To avoid compliance issues, employers should have a clear internal process: verify computations, set a payout schedule that beats the deadline, and file the required 13th-Month Pay Compliance Report with DOLE by 15 January. This important document shows that you have done your part and can save you from unnecessary back-and-forth later.

Common mistakes to watch out for:

- Counting allowances or bonuses as part of basic pay.

- Forgetting to prorate pay for new or resigned employees.

- Failing to update salary changes in the 13th-month pay computation.

- Leaving the payout too close to the deadline and missing it.

Small errors can snowball into compliance issues, but simple systems prevent them. A reliable payroll setup that keeps accurate records and enforces deadlines quietly handles what could otherwise turn into a year-end scramble.

Automating 13th-Month Pay with Smart HR Tools

Managing 13th-month pay is one of the most critical parts of payroll in the Philippines. Between prorated calculations, multiple employee types, and the PHP 90,000 tax exemption ceiling under the TRAIN Law, even small mistakes in 13th-month pay computation can lead to compliance risks and employee dissatisfaction.

With Omni’s all-in-one HR and payroll software, you can automatically track who’s eligible and how to compute 13th-month pay for each employee, apply the correct tax rules, and generate audit-ready reports for DOLE.

Built for growing teams in the Philippines and with local support, Omni streamlines complex statutory requirements into one seamless workflow, giving HR teams the confidence that every payout is accurate and compliant. See how Omni automates 13th-month pay computation and simplifies payroll compliance.

Frequently Asked Questions

Yes, it’s required for all rank-and-file private sector employees who have worked at least one month during the year. It’s a legal obligation under PD 851, not a company perk.

Add up their total basic salary earned until their last working day and divide by 12. This prorated amount should be included in their final pay to stay compliant.

Yes. Probationary employees are entitled to it, prorated based on how many months they’ve worked. As long as there’s an employer-employee relationship, they qualify.

No. The 13th-month pay is mandatory under law; a Christmas bonus is optional and given at the employer’s discretion. Employers can give both, but only one is required.

Yes. It can be released in two parts, as long as the full amount is paid by December 24. Many companies give half mid-year and the rest before Christmas.

Yes. Under the TRAIN Law, the total of 13th-month pay and other bonuses up to 90,000 is tax-free. Anything above that threshold is added to taxable income.

It must be paid on or before December 24 each year. Employers must also file a compliance report with DOLE by January 15 of the following year.

.png)

.png)