Summary. Staying compliant with Singapore’s evolving CPF contribution rates is critical for every employer. With the CPF contribution rate 2025 raising contributions for employees aged 55 to 65 and the CPF ceiling 2025 increasing to S$7,400 (up from the CPF ceiling 2024 of S$6,800), payroll teams must carefully manage both employer CPF contributions and employee CPF contributions to avoid errors. These CPF changes directly impact manpower costs, take-home pay, and long-term planning, especially with another increase to the CPF salary ceiling coming in 2026. By understanding the full CPF contribution table, including ordinary wages, additional wages, and the CPF contribution cap, HR leaders can avoid costly mistakes and maintain employee trust. With Omni, the latest CPF contribution 2025 rules — from CPF percentage updates to automatic CPF contribution statements — are seamlessly built into payroll, ensuring compliance while giving you confidence in every CPF calculation.

The Central Provident Fund is an essential aspect for both employers and employees. Singapore employers face increasingly complex CPF contribution rates, especially with the CPF contribution rate 2025 changes affecting payroll and HR budgeting.

Mismanaging employer CPF contribution or employee CPF contribution can lead to costly compliance penalties and payroll errors. Most guides only cover high-level rates and ignore details like CPF ceiling 2025, CPF cap, and employee-specific scenarios.

In this guide, we provide a complete overview of CPF contribution 2025, CPF contribution history, CPF contribution ceiling, and how Omni can help you plan and adapt to CPF changes 2025 and beyond.

Importance of CPF Compliance and Planning

Every payroll manager in Singapore keeps a close eye on CPF contribution rates as even a one-point change can affect both company costs and employee expectations. The employer CPF contribution is a direct line in your budget, while the employee CPF contribution shapes take-home pay and employee trust.

In 2025, the stakes are higher. With CPF changes 2025, older workers are contributing more, and the higher CPF contribution cap (monthly ceiling at S$7,400) means high earners are affected too.

When CPF is mishandled, the impact goes beyond compliance notices. Errors trigger fines, force messy retroactive adjustments, and can erode employee confidence. On the other hand, companies that plan for shifts like the move from the CPF contribution rate 2024 to the CPF rate 2025 avoid surprises and build trust with their teams.

Omni tip: The CPF Ordinary Wage ceiling will be increased from S$7,400 to S$8,000 starting 1 January 2026, while the annual salary ceiling remains unchanged at S$102,000.

Key things you need to keep in mind as an employer:

- Staying on top of CPF contribution rates keeps your payroll accurate and compliant.

- The CPF employer contribution directly increases your manpower costs each year.

- The higher CPF contribution cap in 2025 and beyond affects budgeting for your high earners.

- CPF changes 2025 raise contribution rates for employees aged 55 to 65, effective January 2026.

- A smooth shift from the CPF contribution rate 2024 to 2025 requires updated payroll systems and clear communication with your staff.

Many Singaporean employers are turning to payroll automation and compliance tools to stay on top of these changes. Building CPF rules into your systems means fewer manual fixes and more confidence that you’re meeting both compliance requirements and employee expectations.

Detailed CPF Contribution Rate 2025 Breakdown

To see how the CPF contribution rates 2025 play out in practice, let’s walk through the rules using one employee as an example. This will connect the dots across age brackets, ceilings, PR status, and historical shifts.

1. Age brackets and CPF rates

CPF contribution rates are tiered by age. Younger employees contribute more as the government wants them to build their CPF Ordinary Account (CPF OA contribution) early, while older workers still save but at a lighter rate.

From January 2025, the official CPF rate 2025 is:

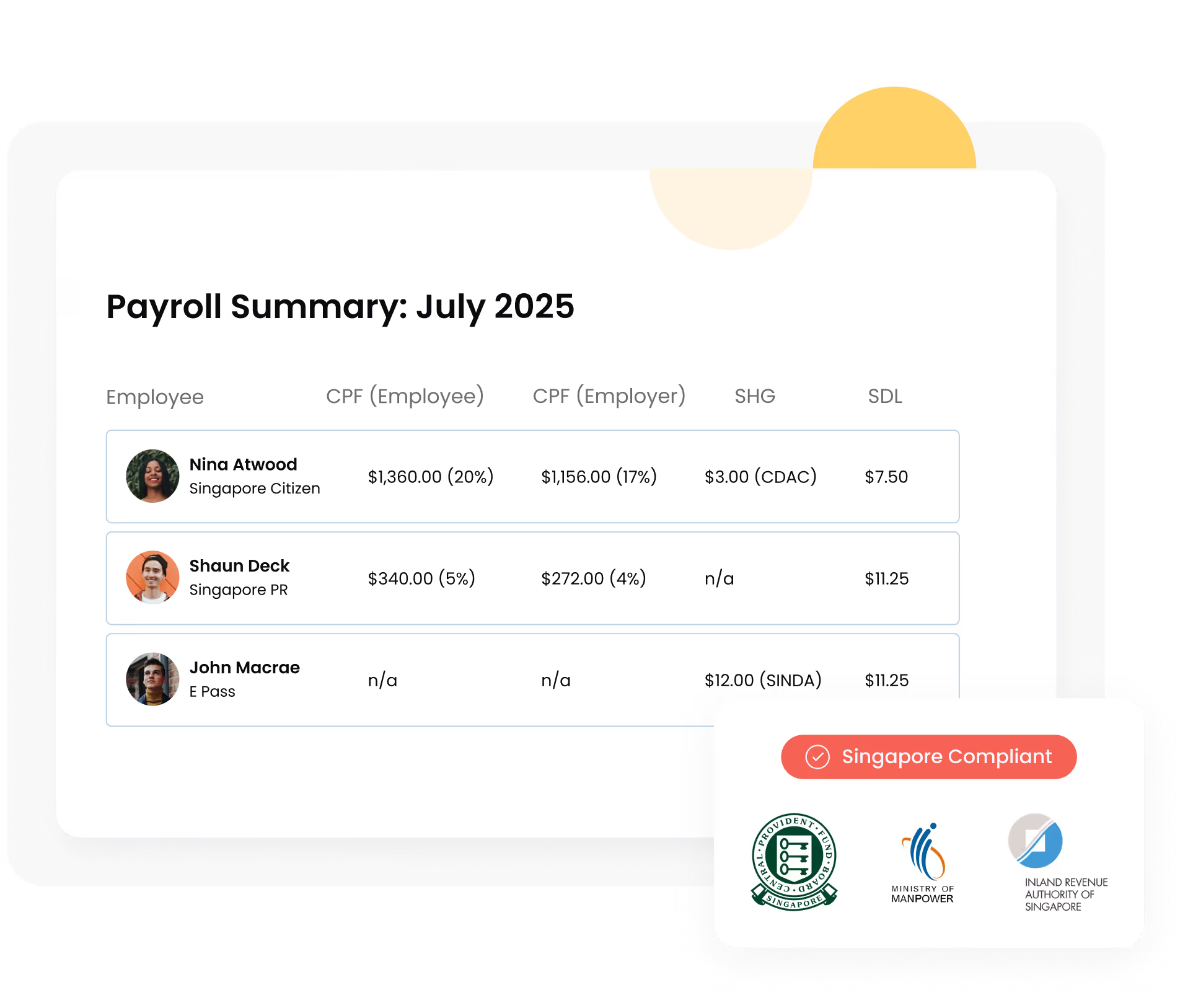

For example, Mr Tan is a 54-year-old Singaporean citizen earning S$8,000 a month. Even though his salary is S$8,000, CPF contributions are not based on the full amount. This is due to the CPF monthly salary ceiling 2025, which is capped at S7,400. So, CPF is only calculated on S$7,400.

In his age group, the CPF contribution rates 2025 are:

- Employer CPF contribution: S$1,258 (S$7,400 x 17%)

- Employee CPF contribution: S$1,480 (S$7,400 x 20%)

- Total CPF contribution: S$2,738

When Mr Tan turns 56, his CPF contributions will automatically adjust because the CPF rate 2025 for his age band is lower. From that month onwards:

- Employer CPF contribution: S$1,147 (S$7,400 x 15.5%)

- Employee CPF contribution: S$1,258 (S$7,400 x 17%)

- Total CPF contribution: S$2,405

This example highlights how CPF changes with age. Payroll teams need to track birthdays carefully, as the CPF contribution rate 2025 and beyond updates immediately in the next month’s salary.

2. Monthly wage ceiling and contribution caps

The CPF ceiling 2025 has increased to S$7,400, and as noted above, will increase again to S$8,000 starting 1 January 2026. This acts as the CPF monthly salary ceiling or CPF cap for ordinary wages.

CPF also treats different types of wages differently:

- Ordinary Wages (OW): This refers to a fixed monthly salary, and it is subject to the CPF monthly salary ceiling 2025 of S$7,400.

- Additional Wages (AW): This includes bonuses, commissions, and other variable payments. These are subject to the annual CPF contribution cap of S$102,000 (including both OW and AW).

In short, the CPF ceiling 2025 and the annual CPF contribution cap work together to set the maximum CPF contribution an employee can receive in a year.

Using the same example above:

- Mr Tan’s ordinary wages are capped at the CPF monthly ceiling of S$7,400. Over 12 months, this adds up to S$88,800.

- If he gets a S$20,000 bonus at the end of the year, CPF contributions don’t apply to the full bonus. Instead, only S$13,200 counts due to the annual CPF contribution cap of S$102,000 (S$88,800 + S$13,200).

- The remaining S$6,800 of the bonus is CPF-free.

This is why Singapore payroll teams must keep ordinary wages and additional wages separate. They are capped under different CPF rules, and mixing them up is one of the most common payroll mistakes.

3. Employee type scenarios

CPF contribution rules also depend on the type of employee. Citizens and PRs in their third year or later contribute at the full rates. But PRs in their first two years have reduced contributions, and foreigners on work passes don’t contribute at all.

Learn more: PR CPF Contribution Rates in 2025: What Employers and New PRs Should Know

Using the same Mr Tan example:

- If he had just become a PR in 2025 (1st year), his CPF contributions would be much lower. On the S$7,400 monthly CPF ceiling, the employer contributes S$296 and the employee contributes S$370, making it a total of S$666.

- As a Singapore Citizen or PR from the 3rd year onwards, the same ceiling would mean S$1,258 from the employer and S$1,480 from the employee, totalling S$2,738.

- By the 3rd year of PR, Mr Tan would be paying the full CPF contribution rates, the same as a citizen.

Managing the difference in CPF contribution rates between Singapore Citizens and PR can be tricky. HR teams often miss the point when a PR transitions from the graduated CPF contribution rates in the first two years to the full rates from the third year onward.

With HR tools like Omni, these statutory contributions, including CPF employer contributions and employee CPF contributions, are automatically adjusted based on the PR’s status, reducing errors and saving valuable time.

4. Historical context

In 2024, the total CPF contribution rate for employees aged 55 to 60 was 31%, and for those aged 60 to 65, it was 22%.

With the new CPF rate 2025, these moved up to 32.5% and 23.5%. Workers aged 55 and below, and those above 65, kept the same CPF percentage.

The CPF ceiling 2024 was S$6,800. In 2025, the ceiling rose to S$7,400, and by 2026, it will reach S$8,000. For someone like Mr Tan, earning S$8,000 a month, that means:

- In 2024, CPF was only calculated on S$6,800.

- In 2025, CPF is calculated on S$7,400.

- In 2026, the full S$8,000 will be CPF-liable.

The CPF contribution history shows a clear pattern: contribution rates for older employees and the CPF salary ceiling for higher earners are going up steadily. For employers, this means adjusting payroll systems early, because each change raises CPF employer contributions in a predictable but unavoidable way.

CPF Rate Comparison: 2024 vs 2025

Looking at the CPF contribution rates side by side helps payroll teams spot the pressure points. With the new CPF contribution rate 2025, two big changes stand out:

- Higher contribution percentages for employees aged 55 to 65 (from 31% to 32.5%, and from 22% to 23.5%).

- A higher CPF salary ceiling — moving from the CPF ceiling 2024 of S$6,800 to the CPF ceiling 2025 of S$7,400, with another increase to S$8,000 in 2026.

Here’s the updated CPF contribution table comparing 2024 and 2025:

Why do these CPF contribution rates matter to your payroll team?

- CPF annual limit unchanged: The maximum CPF contribution remains at S$37,740 per year, while the annual CPF salary ceiling is still S$102,000. But because the CPF ceiling 2025 is higher, more of each employee’s monthly salary is CPF-liable, especially for higher earners. This directly affects both the employer CPF contribution and the employee CPF contribution.

- Greater risk of payroll errors: When the CPF rate 2025 and ceilings shift, payroll teams may misapply the CPF contribution table or confuse ordinary wages with additional wages. Errors in the CPF contribution statement can lead to over- or under-contributions.

- Automation reduces mistakes: With payroll tools like Omni, the latest CPF changes 2025, including updated CPF percentage, CPF contribution cap, and CPF monthly salary ceiling, are already built in. This ensures that every CPF contribution 2025 is calculated correctly, capped at the right limits, and reflected in reports automatically, making the transition from the CPF contribution rate 2024 and beyond seamless for both employers and employees.

Preparing for 2026 Changes

If 2025 feels like a big year for CPF, 2026 will be just as important. The Singapore government has confirmed further CPF contribution rate and CPF ceiling changes taking effect from 1 January 2026, and employers need to prepare for adjustments that impact both budgets and compliance.

What’s coming in 2026

- Higher CPF contribution rates for older workers: For employees aged 55 to 65, total CPF contribution rates will increase by 1.5%. The employer's CPF contribution share increased by 0.5%, while the employee’s share will go up by 1%.

- Bigger CPF salary ceiling: The CPF ceiling 2025 of S$7,400 will rise to S$8,000 per month in 2026, meaning more high earners’ salaries are CPF-liable.

- Cumulative effect of CPF contribution 2025 + 2026: For employees in the 55–65 bracket, the combined incremental increases over both years are significant. Payroll teams should include these in their longer-term manpower and financial planning, not just year-to-year adjustments.

Step-by-step transition planning for smooth compliance

- Review workforce demographics: Look closely at how many employees you have between 55 and 65. This is where the next wave of higher CPF rates will hit hardest.

- Reforecast manpower costs: Update your 2026 budget to reflect the new CPF contribution cap and the additional CPF employer contribution. Even small percentage changes multiply quickly across larger workforces.

- Check your payroll system early: Make sure your HRIS or payroll software automatically reflects the 2026 rules. This includes applying the S$8,000 monthly ceiling and updated age-band percentages.

- Communicate with employees: Staff in their late 50s and early 60s will notice lower take-home pay when their employee CPF contribution rises again. Clear communication will prevent confusion and build trust.

- Run transition checks: In late 2025, run sample calculations using the 2026 CPF contribution rates. This step ensures you won’t be caught by surprise when January payroll rolls around.

Planning saves you the scramble. When you prepare for CPF adjustments early, beyond staying compliant, you’re showing employees you care about their future. With Omni handling the upcoming changes automatically, contributions stay accurate and transitions stay smooth.

CPF Compliance Made Easy with Omni

Keeping track of changing CPF contribution rates can be confusing for Singaporean HR teams. Between the updated CPF contribution rate 2025, the higher CPF ceiling 2025, and future increases to the CPF salary ceiling, it can be easy to make payroll errors. Misapplying an employer's CPF contribution or forgetting to adjust an employee's CPF contribution after a birthday can result in inaccurate payments and compliance risks.

With Omni, CPF compliance is made easy:

- Automated CPF calculations: Apply the right CPF rate 2025 instantly across all employees and age groups, without manual tracking of CPF changes 2025.

- Built-in reporting: Generate accurate CPF contribution statements and review the full CPF contribution table at any time, with no errors.

- Ceiling and cap management: Omni automatically applies the CPF monthly salary ceiling (S$7,400 in 2025) and the upcoming CPF contribution ceiling 2026 of S$8,000, ensuring CPF is calculated only up to the correct CPF cap.

- Integration across HR: Connect payroll, time-off, and attendance so that every CPF employer contribution and employee CPF contribution is correct and compliant.

- Local expertise: Our local support and implementation team provides guidance on CPF contribution history, upcoming rate changes, and compliance best practices.

What sets Omni apart is not just CPF Compliance. Omni’s modern all-in-one HR platform is built for growing teams in Singapore and beyond. With an intuitive interface, award-winning usability, and enterprise scalability, Omni replaces outdated legacy systems with a smarter, faster, and fully compliant HR experience.

“Omni provided us with a unified platform that integrated all essential HR functions into a single system. Payroll, leave tracking, and CPF contributions are now seamless.”

— Wenna Lee, HR Manager at IHRP

With Omni, you’ll never miss a CPF contribution rate update, a CPF ceiling increase, or a birthday-based adjustment again. Try our free CPF calculator to see exactly how much CPF contribution applies to your employees, or book a demo with our team today.

.png)

.png)