Summary. 1 July 2026 marks one of the most significant compliance dates APAC HR teams have faced in recent years. In Australia, the Payday Super reform takes effect, fundamentally changing how employers pay superannuation — from quarterly to every pay run. In Singapore, four changes land simultaneously: the retirement and re-employment ages increase, the Progressive Wage Model expands to admin staff and drivers, the Local Qualifying Salary rises, and EP and S Pass qualifying salaries go up. Vietnam shifts to quarterly PIT filing and raises its statutory base salary, lifting the Social Insurance contribution cap. Meanwhile, Thailand's Employee Welfare Fund — deferred from last year — is confirmed for 1 October, giving HR teams one quarter to prepare. And in India, state-level rollout of the Four Labour Codes continues with the 50% wages rule and fixed-term gratuity changes now in force. This edition covers everything your team needs to know and act on before Q3 closes.

What Are the Key HR Compliance Changes in APAC for Q3 2026?

The major Q3 2026 compliance changes across APAC are:

- Australia: Payday Super requires super contributions with every pay run from 1 July 2026

- Singapore: Retirement age increases to 64, re-employment age to 69; Progressive Wage Model expands to admin staff, drivers, and retail workers; Local Qualifying Salary rises to S$1,800; EP and S Pass qualifying salaries increase — all from 1 July 2026

- Malaysia: Lindung 24 Jam (Non-Employment Injury Scheme) now mandatory for all foreign workers — employers must deduct and remit 0.75% of monthly wages per foreign worker from 1 June 2026

- Philippines: Davao Region (XI) minimum wage second tranche — non-agriculture daily rate rises to PHP 540 from 1 September 2026; employers with multi-region operations should audit all applicable regional wage orders

- Vietnam: PIT filing shifts from monthly to quarterly for all companies from 8 May 2026; statutory base salary rises from 1 July 2026, lifting the Social Insurance contribution cap

- Thailand: Employee Welfare Fund mandatory contributions begin 1 October 2026

- India: Four Labour Codes continue rolling out at state level; the 50% wages rule and fixed-term gratuity changes are in force

Q3 2026 Compliance Snapshot

Australia

Key Updates

- Payday Super — effective 1 July 2026

- SBSCH closure — effective 30 June 2026

What is Payday Super and when does it start?

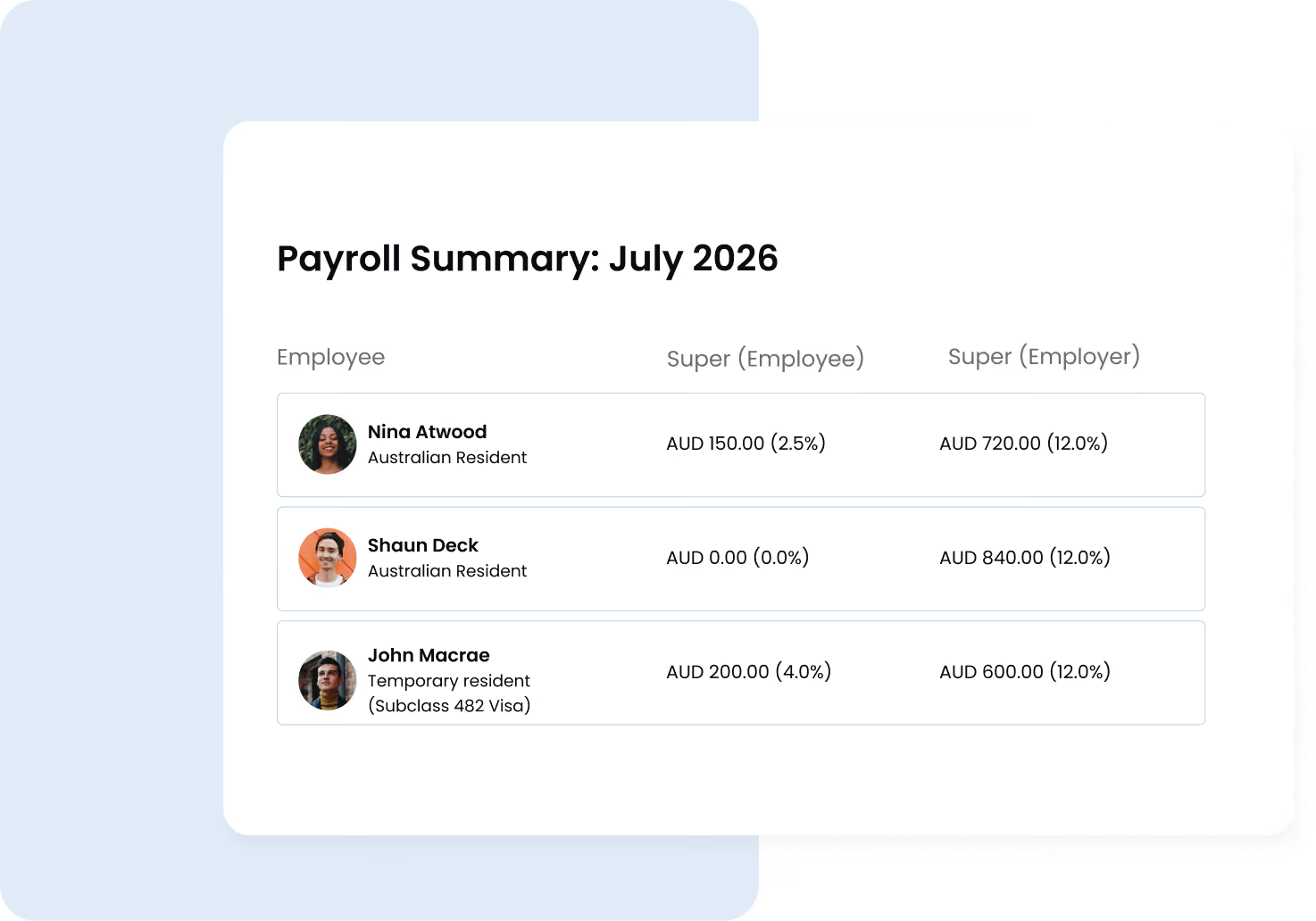

Payday Super is Australia's new requirement for employers to pay superannuation guarantee contributions at the same time as wages, rather than quarterly. It starts on 1 July 2026 and applies to all Australian employers.

This is the most operationally significant payroll change in Australia in decades. Under the current system, super can be paid quarterly, up to 28 days after the end of each quarter. From 1 July 2026, super contributions must reach the employee's nominated fund within 7 business days of payday.

Learn more: Navigating Payroll and Superannuation in Australia

What changes under Payday Super?

Super guarantee is now calculated on "qualifying earnings" — a new term that brings together ordinary time earnings and other payments. While largely aligned with the current OTE rules, the terminology change means payroll systems need to be explicitly updated.

What happens to the ATO Small Business Clearing House?

The ATO Small Business Superannuation Clearing House (SBSCH) closes on 30 June 2026. If your business currently uses it, migrating to a commercial clearing house before that date is urgent — you cannot use the SBSCH for a single pay run from 1 July.

What are the penalties for missing the 7-day super deadline?

From 1 July 2026, any employer who does not pay superannuation in full and on time will be required to pay the updated Superannuation Guarantee Charge, with penalties reaching up to 25% or 50% of the unpaid amount. The ATO will use Single Touch Payroll data matched against fund receipts to identify late payments automatically.

Action required:

- Confirm your payroll software is updated for per-payday super payments and QE calculations

- Migrate off the SBSCH before 30 June 2026

- Ensure STP Phase 2 reporting is active and correctly configured

- Test that contributions can reach super funds within 7 business days, accounting for clearing house processing time

How Omni Helps

Automate your super calculations for each pay run, generate compliant reports, and track super payment status per employee to keep you inside the 7 business day window.

Singapore

Key Updates

- Retirement & re-employment age increase — effective 1 July 2026

- Progressive Wage Model: admin staff & drivers — effective 1 July 2026

- Local Qualifying Salary increase — effective 1 July 2026

- EP & S Pass qualifying salary increase — effective 1 July 2026

- Progressive Wage Model: retail workers — effective 1 September 2026

1. Retirement and Re-employment Age Increases

What is Singapore's new retirement age from July 2026?

From 1 July 2026, the retirement age increases from 63 to 64, and the re-employment age rises from 68 to 69. This keeps Singapore on track toward the 2030 targets of 65 and 70, respectively.

Employers must offer eligible employees yearly renewable contracts from age 64 to 69, or provide a one-off Employment Assistance Payment (EAP) as a last resort.

The Senior Employment Credit will be extended until December 2027, with the highest wage support tier of 7% applying to workers aged 69 and above, helping businesses manage the cost of retaining experienced senior employees.

Action required:

- Identify all employees turning 64 in Q3–Q4 2026 and issue re-employment offers at least 3 months before their birthday

- Update employment contract templates and internal HR policies

- Brief line managers on their obligations before 1 July

- Review succession planning strategies for affected roles

How Omni Helps

Track employee birth dates, trigger automated re-employment offer reminders, and generate reports on employees who are approaching the new retirement age.

2. Progressive Wage Model: Admin Staff, Drivers, and Retail Workers

Which roles does the Progressive Wage Model cover from July 2026?

From 2026, the Occupational Progressive Wages plan expands to include administrative staff and drivers, and the retail sector, one of the biggest PWM expansions since the model began.

About 43,800 administrators and 12,900 drivers in firms that employ foreign workers can expect wage increases from 1 July 2026.

From 1 July 2026 — admin staff:

From 1 July 2026 — drivers:

From 1 September 2026 — retail workers:

Wage progression is linked to WSQ training requirements, and employees in covered roles must complete relevant Workforce Skills Qualification modules to move up the pay ladder.

Action required:

- Identify all Singapore citizens and PR employees in covered admin, driver, and retail roles

- Benchmark current wages against the new OPW minimums

- Implement wage adjustments by 1 July for admin/driver roles and 1 September for retail roles

- Track WSQ training completion for all covered employees

How Omni Helps

Flag-covered employees earning below the new OPW thresholds, track training completion alongside wage progression, and automate salary update workflows ahead of each effective date.

3. Local Qualifying Salary Increase

What is the new Local Qualifying Salary from July 2026?

From 1 July 2026, the Local Qualifying Salary for full-time local employees increases from S$1,600 to S$1,800.

The LQS determines whether a local employee counts toward your Work Permit and S Pass foreign-worker quotas. Any local employee earning between S$1,600 and S$1,799 will no longer count as a full local worker in your quota entitlement, directly affecting how many foreign workers your company is entitled to hire.

Action required:

- Audit all local employee salaries against the new S$1,800 threshold

- Identify employees in the S$1,600–S$1,799 range and assess the quota impact

- Adjust foreign worker headcount planning for Q3 onwards

How Omni Helps

Omni's Singapore payroll automatically applies the updated LQS and flags employees whose earnings affect your foreign worker quota entitlement. Use our CPF calculator for quick salary checks.

4. EP and S Pass Qualifying Salary Increases

What are the new Employment Pass and S Pass minimum salaries from July 2026?

The Employment Pass minimum qualifying salary increases from S$5,600 to S$6,000 for the general economy, and from S$6,200 to S$6,600 for the Financial Services sector. The S Pass minimum qualifying salary rises from S$3,300 to S$3,600 for the general economy, and from S$3,800 to S$4,000 for the Financial Services sector.

Qualifying salaries continue to increase progressively with age, up to S$11,500 for EP holders and S$5,100 for S Pass holders in their mid-40s.

Action required:

- Review all EP and S Pass holders and pending applications against the new salary thresholds

- Adjust compensation packages where needed before submitting renewals or new applications

- Update employment contracts and job offer templates

Malaysia

Key Updates

- Lindung 24 Jam mandatory for all employers with foreign workers — effective 1 June 2026

What is Lindung 24 Jam?

Lindung 24 Jam is PERKESO's Non-Employment Injury Scheme, a new mandatory social security protection for foreign workers in Malaysia that took effect on 1 June 2026. Unlike the existing Employment Injury Scheme (which covers accidents during working hours), Lindung 24 Jam extends coverage to accidents that happen outside of working hours and are not related to the employee's job or duties.

Prior to this scheme, a foreign worker injured in a road accident or domestic incident outside of work had no SOCSO protection. Lindung 24 Jam closes that gap.

Who does it cover?

Lindung 24 Jam applies to all foreign workers with valid work passes, including Visit Pass (Temporary Employment), Employment Pass, Special Pass, and other valid work permits. It applies to all sectors. Domestic workers are covered under a separate PERKESO scheme.

What are the contribution obligations?

Contributions are fully borne by the employee. The employer's role is to deduct the contribution from wages and remit it to PERKESO on the employee's behalf, for as long as the employee remains in their employment. Rates are phased in over three periods:

Contributions are calculated based on the employee's monthly wages.

What are the penalties for non-compliance?

Failure to register foreign workers or remit Lindung 24 Jam contributions is an offence under the Employees' Social Security Act 1969. Convicted employers face a fine of up to RM10,000, two years imprisonment, or both.

What does an employer need to do?

If you have already registered your foreign workers under PERKESO's existing Employment Injury and Invalidity schemes, Lindung 24 Jam contributions are added to the same monthly contribution process. The additional deduction should appear automatically when you submit via the ASSIST portal.

Action required:

- Confirm that all foreign workers with valid work passes are registered with PERKESO under the Lindung 24 Jam scheme from 1 June 2026

- Update payroll to deduct 0.75% of monthly wages per foreign worker and remit through PERKESO's ASSIST portal

- Verify your payroll system reflects the correct phased rate structure

- Communicate the new deduction to affected foreign workers

How Omni Helps

Omni's Malaysia payroll automates EPF, SOCSO, and EIS contribution calculations. Lindung 24 Jam deductions and remittances for foreign workers are managed within the same payroll workflow, keeping your PERKESO contributions accurate and audit-ready.

Philippines

Key Updates

- Davao Region (XI) minimum wage second tranche — effective 1 September 2026

What is changing with the Philippines minimum wages in Q3 2026?

The Philippines does not operate a single national minimum wage. Regional Tripartite Wages and Productivity Boards (RTWPBs) set wage floors by region, and many 2026 wage orders were structured in two tranches, with the second tranche landing across Q2 and Q3.

The critical Q3 date is 1 September 2026, when the Davao Region (Region XI) second tranche takes effect under Wage Order No. RB XI-24. The non-agriculture daily minimum wage rises from PHP 525 to PHP 540, and the agriculture sector from PHP 515 to PHP 525. This directly affects around 66,772 minimum wage earners in the region.

Are there other regional increases to watch?

Several other regions implemented second-tranche increases earlier in 2026 — Northern Mindanao (Region X) and Caraga (Region XIII) in May, and Eastern Visayas (Region VIII) and Zamboanga Peninsula (Region IX) in June. If your operations span multiple regions, audit each one separately against the applicable RTWPB wage order.

Employers should also be aware of potential wage distortion, where mandatory minimum wage increases compress the gap between salary levels across different employee tiers. The NWPC advises employers to review and correct distortions proactively when new wage orders take effect.

Action required:

- Update payroll for Davao Region (XI) employees from 1 September 2026 to reflect the new PHP 540/day non-agriculture rate

- Audit all Philippine regions where you have employees against the current RTWPB wage orders

- Check for and address wage distortion across salary tiers following any minimum wage increase

How Omni Helps

Manage the Philippines payroll across multiple regions in one platform, apply the correct regional wage floor per employee location, and generate compliance reports for DOLE audit readiness. Use our SSS calculator for quick contribution checks.

Vietnam

Key Updates

- PIT filing shifts from monthly to quarterly — effective 8 May 2026

- Statutory base salary increase, lifting the Social Insurance cap — effective 1 July 2026

What is changing with Vietnam's PIT filing frequency?

The Ministry of Finance has issued Decision No. 1109/QD-BTC, introducing a key change to the filing frequency for Personal Income Tax (PIT) on salary and wage income. Under this regulation, filings shift from a monthly to a quarterly basis, effective 8 May 2026.

This applies to all companies, regardless of whether annual turnover is below or above VND 50 billion — the threshold that previously distinguished filing frequency for many businesses. If your finance or payroll team has been filing PIT monthly, this changes your compliance calendar materially.

Action required:

- Confirm with your finance or payroll team that PIT filing has moved to a quarterly cadence from 8 May 2026

- Update internal compliance calendars and reconciliation processes to reflect the new filing schedule

- Notify your tax or accounting provider if PIT filing is outsourced

What is changing with Vietnam's statutory base salary?

Under Decree No. 161/2026/ND-CP, Vietnam's statutory base salary rises from VND 2,340,000 to VND 2,530,000 per month, effective 1 July 2026.

While the base salary primarily governs public-sector pay, it also sets the contribution ceiling for Social Insurance (SI) and Health Insurance (HI) in the private sector. Under Vietnam's compulsory insurance framework, the maximum salary subject to SI and HI contributions is capped at 20 times the statutory base salary.

Employers with employees earning at or near the previous cap of VND 46,800,000 will see increased SI, HI, and trade union contribution obligations from July payroll onward. The increase also affects trade union dues, which are calculated as a percentage of the same salary base.

Action required:

- Identify employees earning at or near the previous SI/HI contribution cap of VND 46,800,000/month

- Update payroll systems to apply the new VND 50,600,000 contribution ceiling from 1 July

- Recalculate employer SI, HI, and trade union contribution costs for affected employees

- Communicate any payroll deduction changes to affected employees ahead of July payroll

How Omni Helps

Automatically apply the updated SI/HI contribution ceiling from 1 July, recalculate employer and employee contributions for affected employees, and keep your PIT filing calendar aligned with the new quarterly cadence.

Thailand

Key Updates

- Employee Welfare Fund mandatory contributions — effective 1 October 2026

What is Thailand's Employee Welfare Fund?

The Employee Welfare Fund (EWF) is a new mandatory savings scheme that provides a lump-sum payment to employees upon termination, retirement, or death. It is established under Section 126 of Thailand's Labour Protection Act B.E. 2541 (1998).

The Thai Cabinet approved a one-year postponement of mandatory EWF contributions, moving the start date from 1 October 2025 to 1 October 2026. That window has arrived, and the preparation needs to happen now.

Who must contribute to the Employee Welfare Fund?

Beginning 1 October 2026, both employer and employee must contribute 0.25% of the employee's monthly wages to the EWF. This rate increases to 0.50% from 2031. The mandate applies to all private-sector employers with 10 or more employees.

Does a provident fund exempt you from the EWF?

Yes. Employers who already offer a qualifying registered provident fund under the Provident Fund Act B.E. 2530 (1987) are generally exempt from EWF contributions. Reviewing whether to establish a provident fund before October is worth doing now, as provident fund contributions carry significant tax benefits for both employers and employees, whereas no tax benefits have been announced for EWF contributions.

Action required:

- Determine whether your organisation qualifies for exemption via an existing provident fund

- If not exempt: register employees with the EWF and update payroll systems for the 0.25% deduction from 1 October

- Inform employees of the new deduction in advance

- Budget for the additional employer cost in Q4 2026 financial plans

How Omni Helps

We support payroll in Thailand with automated statutory deduction calculations. EWF contribution tracking and remittance reporting will be available ahead of the 1 October deadline.

India

Key Updates

- Four Labour Codes — state-level rollout — ongoing from April 2026

What is the current status of India's Four Labour Codes in Q3 2026?

India's Four Labour Codes came into effect on 21 November 2025, but full operationalisation awaits final notification of central and state rules, with implementation targeted from April 2026. As of Q3 2026, enforcement is advancing at different speeds across states.

The Four Labour Codes were covered in depth in our Q2 2026 update and our complete India Labour Codes guide. Here's what remains highest-priority heading into Q3.

The 50% Wages Rule

The most impactful provision requires basic pay plus Dearness Allowance to constitute at least 50% of an employee's total CTC. Under the old regime, companies could keep basic salary as low as 20–30% of CTC to reduce PF contributions and gratuity accruals. That is no longer permissible, and the change cascades directly into higher PF contributions and gratuity liabilities.

Fixed-Term Employee Gratuity

The five-year minimum service requirement for gratuity no longer applies to fixed-term employees. A fixed-term worker is entitled to gratuity proportional to their period of service from Day 1, calculated at the standard rate of 15 days' wages per year of service. Employers must provision for this from the first day of any fixed-term engagement.

Action required for Q3:

- Audit salary structures in every operating state to identify employees with basic wages below 50% of gross CTC

- Restructure compensation packages and recalculate PF and gratuity on the updated wage definition

- Provision of gratuity from Day 1 for all fixed-term employees

- Monitor your state's labour department portal for state-specific rule notifications

Stay Compliant and Confident with Omni HR

Managing simultaneous compliance changes across these markets is exactly where manual processes and legacy systems break down.

With Omni, your HR and payroll compliance keeps pace with every regulatory change:

- Automated payroll updates reflect statutory rate and threshold changes across all markets

- Real-time dashboards track pass expiries, wage floors, and re-employment offer deadlines

- Multi-country payroll handles PIT changes, super calculations, and minimum wage adjustments in one place

- Workflow automation sends reminders for EP renewals, OPW training deadlines, and statutory filing cadences

- Audit-ready reporting for labour inspections, government filings, and internal reviews

Schedule your product tour today and see how Omni can simplify your Q3 2026 APAC HR compliance.

Frequently Asked Questions

Australia's Payday Super reform is the most operationally significant change for Q3 2026. From 1 July 2026, Australian employers must pay superannuation contributions with every pay run — not quarterly — and contributions must reach the employee's fund within 7 business days. Late payment penalties can reach up to 200% of the unpaid amount.

Singapore's minimum retirement age increases from 63 to 64, and the re-employment age rises from 68 to 69, effective 1 July 2026. Employers must offer eligible employees re-employment contracts up to age 69, or pay a one-off Employment Assistance Payment. The Senior Employment Credit is extended to December 2027 to help offset costs.

From 1 July 2026, administrators must earn a minimum gross monthly wage of S$2,360, admin executives S$2,940, general drivers S$2,200, and specialised drivers S$2,790. These apply to Singapore citizens and PRs in firms that employ foreign workers, and are tied to WSQ training requirements.

Thailand's Employee Welfare Fund mandatory contributions begin on 1 October 2026 for all private-sector employers with 10 or more employees. Employers and employees each contribute 0.25% of monthly wages. Employers with qualifying registered provident funds may be exempt.

Yes. The Four Labour Codes were notified effective 21 November 2025. The 50% wages rule — requiring basic pay to constitute at least 50% of total CTC — is in force. State-specific rules are rolling out progressively from April 2026, so the enforcement timeline varies by state.

Lindung 24 Jam is fully employee-borne, with employers deducting and remitting on the employee's behalf. Rates are phased: 0.75% of monthly wages in Years 1–2, 1.00% in Years 3–5, and 1.25% from Year 6 onwards. It applies to all foreign workers with valid work passes, effective 1 June 2026.

Two changes land in Q3. First, PIT filing on salary and wage income shifts from monthly to quarterly for all companies from 8 May 2026, under Ministry of Finance Decision No. 1109/QD-BTC. Second, Vietnam's statutory base salary rises to VND 2,530,000 from 1 July 2026, which lifts the Social Insurance and Health Insurance contribution cap from VND 46,800,000 to VND 50,600,000 — increasing employer costs for higher-paid employees.

.png)

.png)