Summary. As Singapore's 1 March 2026 IR8A filing deadline approaches, IRAS has introduced significant changes for YA 2026 that go beyond simple updates; they fundamentally reshape how payroll teams must capture, validate, and submit employee income data. The key changes include tightened reporting requirements with mandatory NRIC/FIN fields and detailed income breakdowns, discontinuation of Form IR8S with voluntary CPF now consolidated into IR8A, mandatory simultaneous filing of Appendices 8A/8B alongside IR8A, combined BIK and ESOW declarations, and a digital-first shift for AIS users directing employees to IRAS myTax Portal. These changes require immediate operational adjustments in payroll systems, data governance practices, and internal review processes. Organizations that fail to prepare adequately risk submission rejections, late filing penalties, and compliance issues. Whether you manage payroll in-house or work with a provider, understanding these changes and implementing proper controls now is critical to avoiding last-minute filing challenges.

As the Global EOR and Payroll Lead in Omni HR working with Singapore-based clients across multiple industries, I’ve seen firsthand how regulatory changes can translate into operational friction.

Every filing season, the same pattern emerges: HR and payroll teams are aware that changes are coming, but the implications on payroll, tax filing processes, and internal review controls are often unclear until it’s time for submission.

The newly introduced YA 2026 IR8A updates are not just small tweaks. They represent IRAS’s shifts in how employee income data must be captured, validated, and submitted. From tightened reporting requirements to removal of IR8S, consolidation of appendices, and BIK/ESOW declarations, these updates highlight the importance of payroll data governance.

With the 1 March 2026 deadline for IR8A Singapore submission quickly approaching, the risk here isn’t just misunderstanding the changes, but underestimating the operational adjustments needed to ensure your organization remains compliant.

In this guide, I will outline what has changed, where we see the most friction across Singapore businesses, what payroll leaders should implement to avoid last-minute filing risk, and how Omni’s payroll software and managed payroll services can help you handle all these changes end-to-end.

Overview of IR8A Singapore Changes for YA 2026

Learn more: Singapore Tax Filing: Complete IRAS & AIS Guide for HR Teams

1. Tightened Reporting Requirements

IRAS has enhanced validation rules and made more fields mandatory to improve data accuracy and reduce filing errors.

What’s changed

New mandatory requirements

- NRIC/FIN required for all employees

- Complete identification details are mandatory

- Detailed income component breakdown required

Stricter validation controls

- Cross-field validation checks

- Income consistency verification

- Employment date validation

Operational impact

From what we are seeing across clients, the biggest friction point is income classification. Many payroll systems were historically configured with broad earning categories. However, YA 2026 and beyond require more granular mapping to ensure accuracy.

Action plan

- Audit employee master data for missing NRIC/FIN

- Verify all identification numbers are valid and current

- Review the payroll system income codes and classification logic

- Ensure all income components are tracked distinctly

- Reconcile payroll totals with finance records before submission

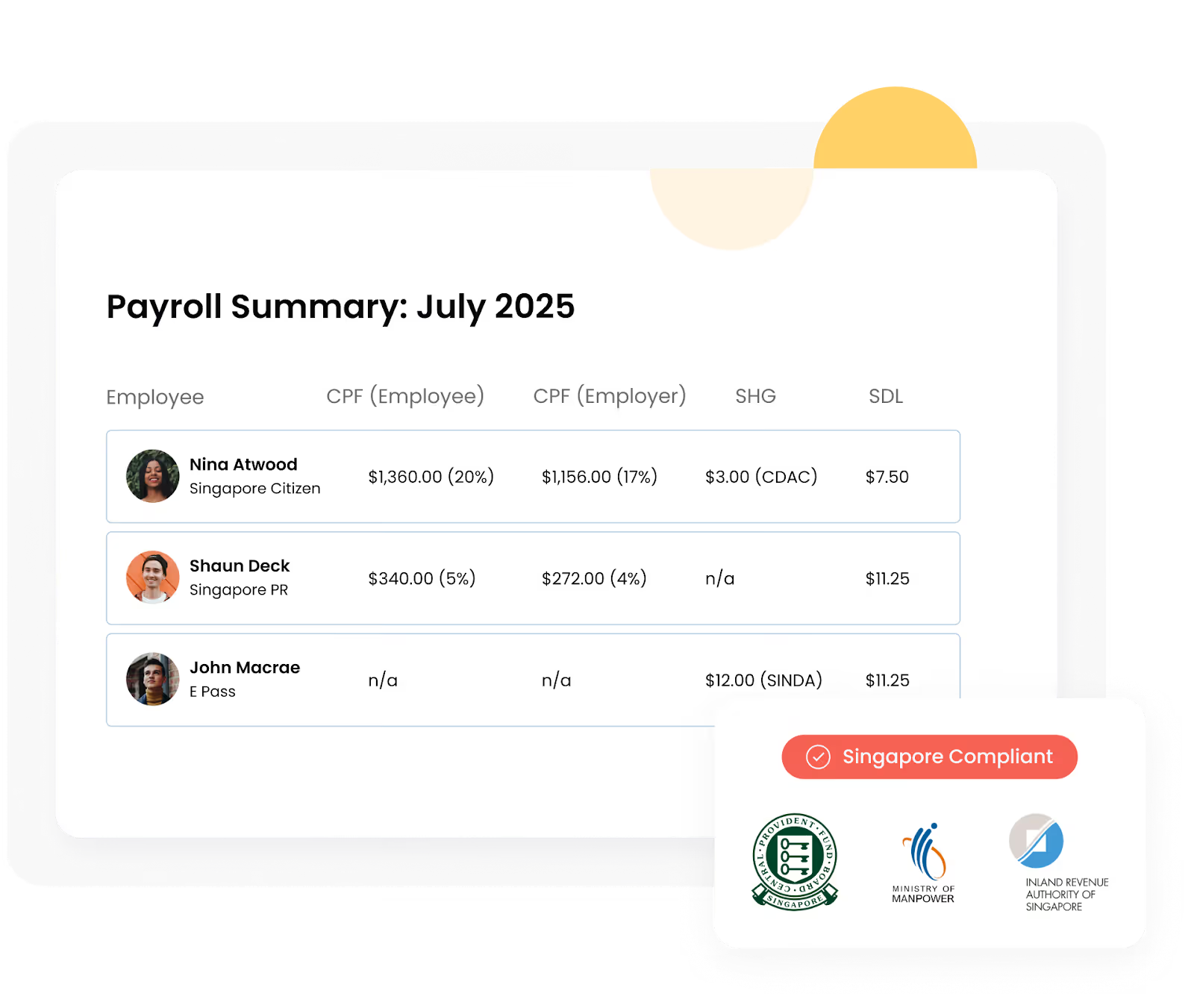

2. Form IR8S Discontinued - Voluntary CPF Now Reported in IR8A

IRAS has removed the separate IR8S form. However, the obligation to report voluntary CPF contributions remains. Voluntary CPF contributions must now be reported directly in the IR8A Singapore form.

What's changed

Previous filing structure: IR8A for regular income + separate IR8S for voluntary CPF

YA 2026: All information consolidated in IR8A form

What counts as voluntary CPF

- CPF top-up programs as employee benefits

- Additional CPF contributions as retention incentives

- Enhanced CPF contributions above mandatory rates

- Special CPF contributions for specific employee groups

Read next: How Omni HRIS Manages CPF Contributions for Singapore Payroll

Where organizations face friction

In many organizations:

- Voluntary CPF is not consistently tagged in payroll systems

- Contributions may be processed manually

- Separation between statutory and voluntary CPF is unclear.

Without clear segregation, reporting errors become likely.

Action plan

- Review 2025 payroll records for voluntary CPF contributions

- Identify employees who received voluntary CPF contributions

- Ensure the payroll system separates voluntary from mandatory CPF in IR8A

- Conduct sample Ir8A test runs before final submission

- Ensure your payroll team understands the revised reporting layout

3. Appendix 8A and 8B Must Be Filed Together with IR8A

Previously: IR8A submitted first, appendices filed separately

YA 2026: IR8A, Appendix 8A, and Appendix 8B must be submitted together in a single filing

When Appendix 8A is required (Benefits-in-Kind):

- Company car for private use

- Housing accommodation

- Interest-free or subsidized loans

- Utilities subsidies

When Appendix 8B is required:

- Directors

- Employees with substantial shareholding

- Individuals receiving specific allowances

Employee coverage matrix

Action plan

- Identify BIK recipients

- Confirm director/shareholder list with the Company Secretary

- Calculate BIK values for all benefits

- Compile all appendix data before starting the IR8A filing

- Create a structured employee-level tracking matrix

Your appendix management should be systematized instead of reactive.

4. Combined BIK and ESOW Declaration

With the new updates, IRAS has officially merged Benefits-in-Kind (BIK) and Employee Stock Ownership/Welfare (ESOW) declarations into a single submission alongside IR8A.

What's included

Benefits-in-Kind (BIK):

- Company vehicles

- Housing benefits

- Utilities subsidies

- Insurance premiums paid by the employer

Read next: Understanding Benefit-in-Kind: A Guide to Employee Benefits in Singapore

Employee Stock Ownership/Welfare (ESOW):

- Stock options exercised

- ESOP distributions

- RSU vesting

- Share awards

Action plan

- Engage finance and equity administrators early

- Confirm all 2025 vesting/exercise events

- Validate valuation methods applied

- Reconcile equity data before submission

5. Employee Communications Change for AIS Users

For organizations under the Auto-Inclusion Scheme (AIS), the IRAS strongly recommends directing employees to the myTax Portal instead of issuing hardcopy IR8A Singapore forms, as it is no longer required.

What employees can view on the portal

- Complete IR8A information

- Auto-populated tax return

- Appendix 8A and 8B details (if applicable)

- Historical tax information

Access methods

- SingPass login

- IRAS PIN (for non-SingPass users)

Communication best practice

Clearly state that:

- IR8A has been submitted via AIS

- Information is available on the IRAS myTax Portal

- How to access the portal

- Who to contact internally for discrepancies

Prepare FAQs in advance, as employee queries typically peak immediately after filing.

Mistakes to Avoid for IR8A Singapore YA 2026 Changes

1. Missing the 1 March deadline

The cost: Late filing penalties, audit triggers, and employee tax filing delays

Best practice: submit before 1 March

- Start data compilation early

- Set an earlier internal deadline

- Build in a 3-5 day buffer

2. Incorrect employee data

The cost: Submission rejection, need to resubmit, risk of missing deadline

Best practice: Verify before submitting

Verification checklist:

- NRIC/FIN matches current documentation

- Name spelling matches government ID

- Employment dates are accurate

- All mid-year changes updated

3. Missing required appendices

The cost: Incomplete filing rejected, resubmission required

Best practice: Track requirements per employee with an employee-level matrix

4. Skipping independent review before submission

The cost: Errors discovered after submission, amendments needed, and audit triggers

Best practice: Implement a two-stage review process

Stage 1 - Self-review:

- All mandatory fields completed

- Income reconciles to payroll

- CPF matches board data

- All appendices attached

Stage 2 - Independent review:

- Spot-check 10-20% against source documents

- Review high-value BIK and equity cases

- Check appendix completeness

How Omni Simplifies Form IR8A Singapore Compliance

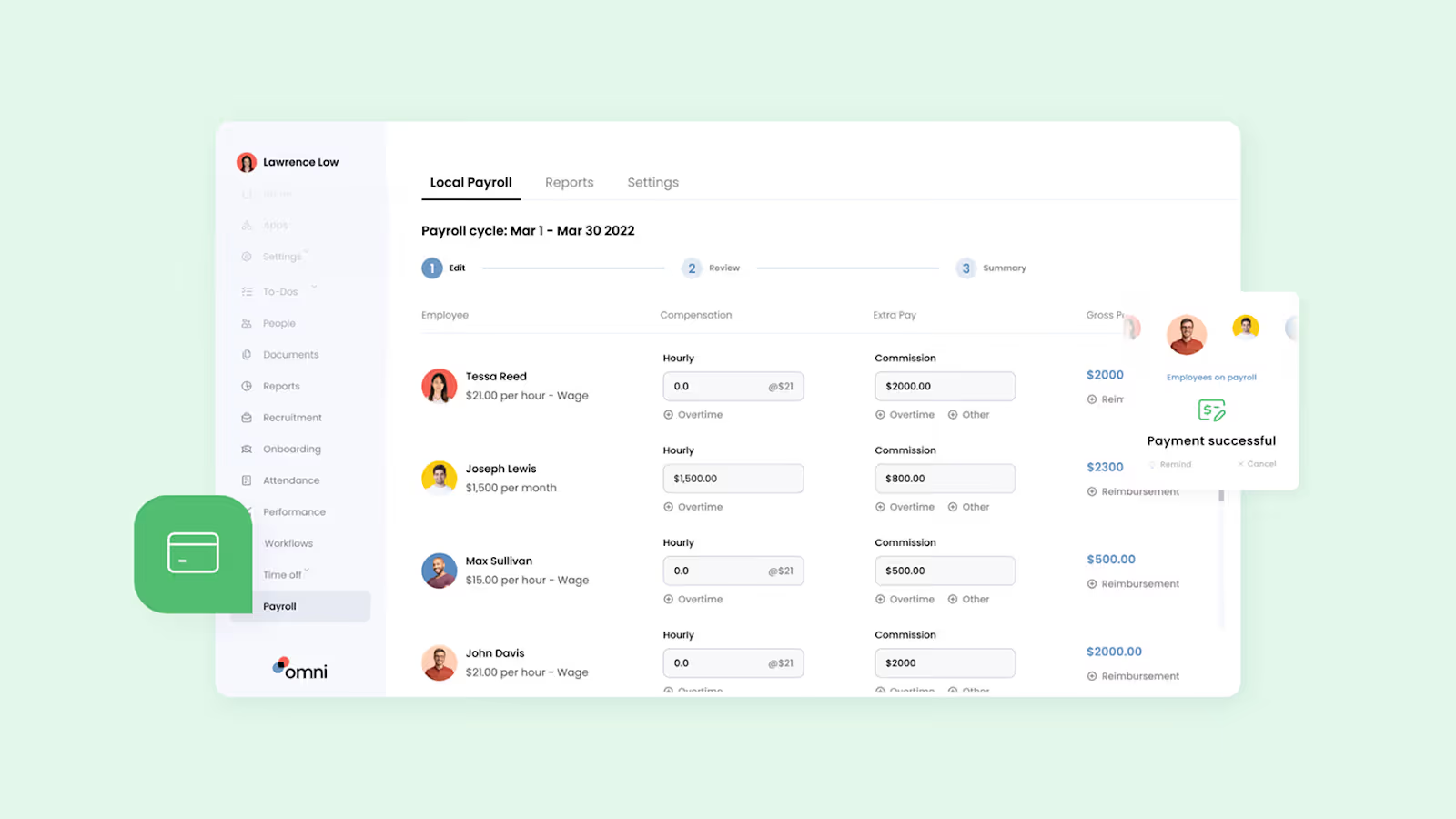

At Omni, we understand that tax compliance shouldn’t be consuming your team’s valuable time. Our platform is fully integrated with IRAS, allowing you to submit employment income electronically directly from your payroll system with just a few clicks.

Manual process vs. Omni HR

How do we achieve this?

The time savings above are only possible due to Omni’s full integration with IRAS and automated compliance features.

Direct IRAS electronic submission

- No manual file exports or separate portal uploads

- Submit employment income directly from Omni to IRAS

- One integrated platform handles everything from payroll processing to tax filing

Automatic YA 2026 compliance

When payroll is set up correctly, all YA 2026 requirements are handled automatically:

- NRIC/FIN validation at data entry - errors are caught even before they become problems

- Detailed income breakdown captured throughout the year

- Voluntary CPF contributions tracked and reported in IR8A format

- Appendix 8A/8B auto-generated based on employee benefits and roles

- Combined BIK & ESOW declaration created automatically

Year-round data capture

Instead of a last-minute scramble, Omni captures everything as and when it happens:

- Every payroll run updates your IR8A data automatically

- Benefits, allowances, and voluntary CPF are tracked in real-time

- Director status and BIK are automatically flagged for the appendix requirements

Your data is ready for you when it’s time for filing, just review and submit.

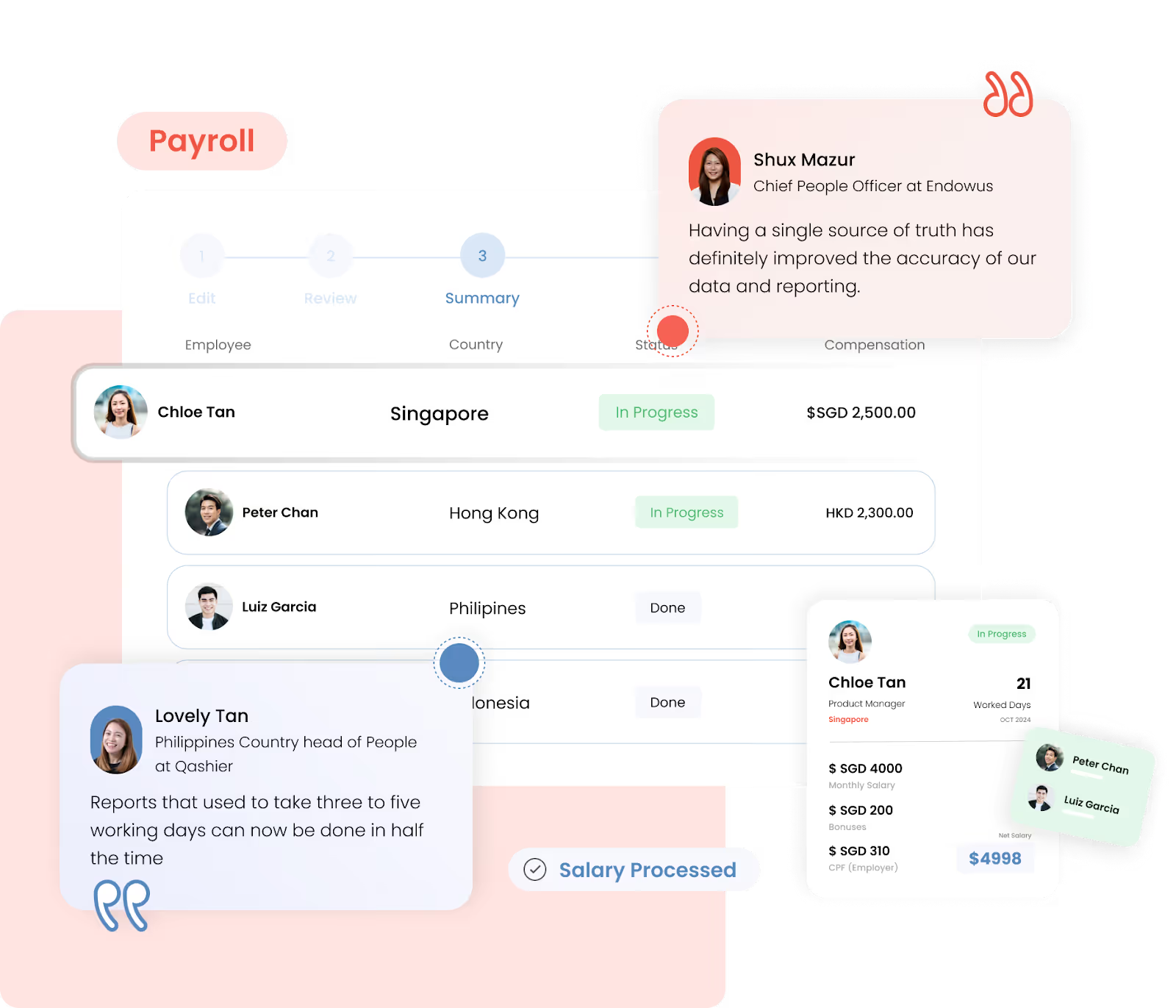

"Payroll calculations that used to take three to five working days can now be done in half the time with Omni."

— Tengku Mohaizad, Group Head of HR Asia at Inspire Brands Asia

Two ways Omni can help your business

Payroll software

- Complete self-service platform

- Manage everything from start to finish

- Run payroll, generate submissions, and file directly to IRAS

- Full control over your compliance process

Managed payroll services

- We handle the entire payroll process for you

- Our payroll experts manage data preparation and validation

- We submit your IR8A filings to IRAS on your behalf

- You review and approve, we execute

Both options leverage the same IRAS-integrated technology, ensuring your payroll operations remain compliant every step of the filing process.

Ready to simplify your tax compliance? Book a demo with our team to see how Omni’s payroll software and managed payroll services can eliminate manual filing work.

.avif)

.avif)

.avif)